- December 9, 2019

- Blog , The Portfolio Strategist - Terry Gardner

C.J. Lawrence Weekly – The Crowd May Be Right

Is there wisdom in the crowd? Market pundits often express concern about the stock market’s “overcrowded trades”, referring to stocks that are owned by a large preponderance of funds and investors. The implication is that investors who own these widely held names are vulnerable to the whims of the crowd (the market). In fact, in periods of stock market volatility, heavily weighted stocks often move with the market, regardless of their organic business strength and relative fundamentals. But over longer periods of time, fundamentals have been shown to drive stock performance. The proliferation of exchange-traded and index funds has probably contributed to the shorter-term trading phenomenon. As heavy weight stocks perform and appreciate, their influence within capitalization-weighted indices increases. As their index weight increases, investors and funds that track those indices need to own more of them, creating a virtuous cycle.

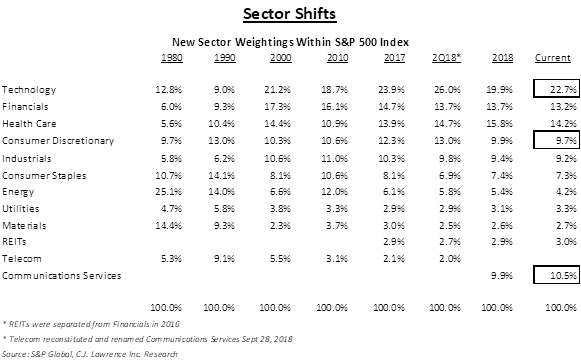

Companies often cited in the “overcrowded” narrative include many well-known technology and consumer companies and are commonly referred to by acronyms like “FAANG” (Facebook, Amazon, Apple, Netflix, and Google (now Alphabet)) or its close relative, “MAGA” (Microsoft, Amazon, Google, and Apple). In fact, as of last week, the category represents four of the top five weighted companies in the S&P 500 Index. Berkshire Hathaway (B class shares) rounds out the top five. As our Sector Shifts table demonstrates, the Technology and Consumer Discretionary (dominated by Amazon.com) stocks gained meaningful market share from 2010 to 2017, and along with the new Communications Services stocks, have driven market performance since being reconstituted in mid-2018.

But avoiding investing in these companies because they are “over-owned” may miss the mark. We screened the S&P 500 Index and scored each constituent on its track record and outlook for sales and earnings growth. Our screen excluded companies that acquired revenues in excess of 25% of prior year sales, and ranked qualifiers based on sales and earnings per share growth over a five-year period (three historic and two forecasted). A heavier emphasis was placed on sales growth since earnings per share can sometimes be influenced by share count and non-cash charges. The result was that many of the “overcrowded” stocks were/are the best financial performers over the five-year period. Among the top 25 leaders are well known stocks like Netflix, Amazon, Facebook, Alphabet, Mastercard, and Microsoft. Also topping the list were Salesforce.com, Adobe, and PayPal. Meanwhile, the other perceived knock on the group, suggesting that “overcrowded” stocks have become increasingly expensive, does not seem to be supported by the data. In fact, the price-earnings multiples of most of the names at the top of the list have come down meaningfully over the past several years as their earnings growth outpaced their share price appreciation. Maybe the crowd is recognizing many of these companies for what they are; innovators and leaders with considerable sales and earning power. The wisdom of the crowd should not be discounted.

Terry Gardner Jr. is Portfolio Strategist and Investment Advisor at C.J. Lawrence. Contact him at tgardner@cjlawrence.com or by telephone at 212-888-6403.