- December 17, 2019

- Blog , The Portfolio Strategist - Terry Gardner

C.J. Lawrence Weekly – Trade Deal and an Earnings Driven Market

Phase I of the U.S. – China trade deal was announced on Friday to much media, but little stock market, fanfare. The adage of “buy the rumor, sell the news” may have been in play. In fact, the S&P 500 Index price is up 5.4% in just the past three months, even as tariff deadlines loomed, in anticipation that some form of a deal would ultimately be reached. After the announcement, the S&P 500 traded flat on the day. The trade deal details are still coming to the surface, but any agreement that buoys international trade would be a positive for the global economy. Like the stock market, equity analysts have also discounted a trade deal, so upward forecast revisions in response are unlikely. China sales account for ~5.8% of S&P 500 constituent company sales, according to FactSet, and less for non-S&P 500 companies. Despite being a top-3 trading partner with the U.S., a return to pre-trade war levels of activity might only juice S&P 500 sales growth by 10-20 basis points. Perhaps more important will be the impact of increased global activity on prices and volumes.

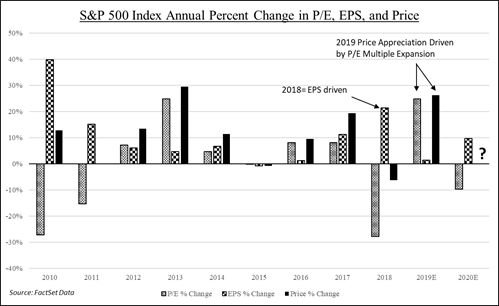

Global economic stability and clarity might finally encourage company managements to invest and pursue growth initiatives. The deceleration in capital spending in 2019 is often cited as a key reason for this year’s punk sales and earnings growth. But analysts concur that the outlook for 2020 is brighter that the 2019 picture. Analysts surveyed by FactSet are forecasting S&P 500 Index earnings per share growth of 9.7% in 2020. Achieving that target may be a critical underpinning to the continued health of the bull market. Stocks have moved higher this year on the back of multiple expansion and there may not be much of that gas left in that tank. Price-earnings multiples are currently within historical norms but are approaching the top of historic ranges. In 2018 the S&P 500 Price Index (excluding dividends) declined 6.2% despite 20+% earnings per share growth, as price-earnings multiples compressed. 2019 saw a flip flop. This year’s earnings will likely come in 1.4% ahead of last year’s level. Yet the S&P 500 price index is up 26.4% year-to-date on the back of multiple expansion.

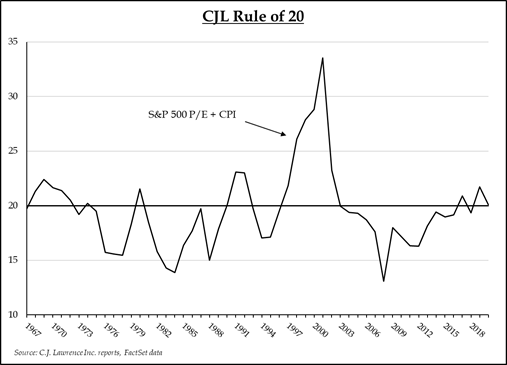

Price-earnings multiples can elevate and remain high during periods of low inflation and low rates of economic growth, so the current level of 17.8x next year’s earnings looks sustainable. Our CJL Rule of 20 tells us that the sum of the forward P/E multiple on the S&P 500 added to the annual CPI core inflation rate should equal about 20. The current reading is 20.1, which sounds about right. Therefore, for stocks to move higher without violating the Rule, the “E” portion of the P/E equation will need to contribute more. That won’t be easy. Current 2020 earnings forecasts call for 5.3% top line growth and a ~50 basis point improvement in net profit margins. S&P 500 sales typically come in 2.0x-2.5x U.S. GDP. Using a 2.0% U.S. GDP growth forecast suggests S&P 500 sales would come in between 4.0%- 5.0%, slightly below current estimates. Meanwhile, using an 18x P/E multiple on next year’s consensus forecasted earnings per share of $177.88 yields an Index price near 3,202 or just 1% higher than current levels. With little room for valuations to expand, the market may need more than a trade deal to ensure the bull’s health.

Terry Gardner Jr. is Portfolio Strategist and Investment Advisor at C.J. Lawrence. Contact him at tgardner@cjlawrence.com or by telephone at 212-888-6403.