- December 2, 2019

- Blog , The Portfolio Strategist - Terry Gardner

C.J. Lawrence Weekly – The U.S. Consumer Remains Healthy, While the Gap Between Sector Winners and Losers is Widening

Most preliminary reports suggest that Black Friday sales were robust, and that Cyber Monday retail activity is expected to reach a new high. The reports dovetail recent U.S. consumer spending reports which continue to paint a picture of a healthy U.S. consumer. Last Wednesday’s Commerce Department report showed that consumer spending grew 0.3% in October, the largest gain since 0.5% in July. The Commerce Department released October retail sales results in the prior week and that report also showed a 0.3% increase. Consumer Confidence ticked down in November but remains at an elevated level. Since domestic consumption accounts for two-thirds of U.S. GDP, a healthy U.S. consumer is an important underpinning to GDP growth. The good news is that the U.S. Consumer remains relatively healthy, wealthy, and wise.

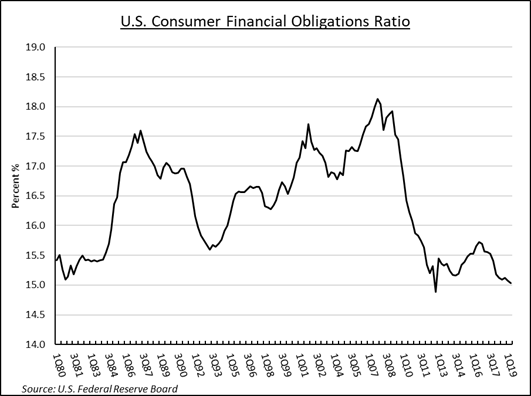

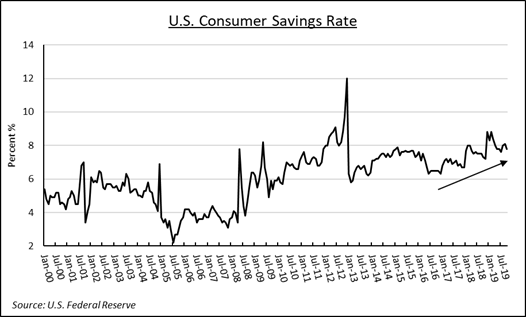

Household wealth grew 1.64% to $113.5 trillion in the second quarter of 2019 according to the Federal Reserve’s flow of funds data. Rising stock prices and rising home values generated much of the increase. At the same time, consumers have been more disciplined borrowers than in past cycles. The Federal Reserve calculates its Financial Obligations Ratio each quarter measuring how much debt consumers are absorbing relative to income. The calculation includes mortgages, consumer debt, rent payments, auto lease payments, homeowners’ insurance, and property tax payments. At the end of the second quarter the ratio stood at 15.08%, the lowest level since it ticked briefly below 15% in 1Q13. Of course, the figures represent an aggregate amount, and it is assumed that the underlying distribution is unequal, but the general trend is quite positive. The same can be said for the U.S. Consumer Savings Rate. High levels of savings are not typical in low interest rate environments, particularly late in an economic cycle. But current savings rates are high and are rising. No irrational exuberance here!

The current backdrop is constructive for consumer related stocks, but investors, like consumers, have been increasingly disciplined and selective. Year-to-date, the S&P Consumer Discretionary Sector Index is up 24.5%. That is slightly below the broader S&P 500 Index performance and there are wide performance dispersions within the sector. The Household Durables sub-group, which contains mostly homebuilders and housing related goods, has appreciated 43.8% this year, followed by the Auto Components group which is up 38.5% during the same period. The sector laggards include the Auto group (+16.7%) and the Internet and Direct Marketing Retail (+18.6%) group. Internet and Direct Marketing Retail underperformance is particularly noteworthy given that group contains Amazon.com, which has historically led the market. Amazon may wind up on Christmas lists of those looking for 2019 laggards with the potential to outperform in 2020. But the starkest dispersion might be found in retail where Target (TGT) can be found in the top 10 performers in the S&P 500, year to date, while Macy’s (M) and Gap Stores (GPS) round out the bottom ten. Like the more financially disciplined U.S. consumers, investors also have become more discriminating. Even within relatively homogeneous groups wide differentials exist. The U.S. consumer is healthy and living within his/her means and that should be positive for consumer related stocks. But wide gaps are forming between those with cutting edge business models and those without. Passive investors in the sector may wind up with average returns, while active investors focused on long-term winners and innovators stand to generate outsized returns.

Terry Gardner Jr. is Portfolio Strategist and Investment Advisor at C.J. Lawrence. Contact him at tgardner@cjlawrence.com or by telephone at 212-888-6403.