- January 7, 2019

- Blog , The Portfolio Strategist - Terry Gardner

C.J. Lawrence Weekly – Stock Price-to-Earnings Ratios May Have Bottomed

The daily whipsaw of the stock market is challenging the convictions of both bulls and bears. 3% intraday moves in index prices have become the norm and the CBOE Volatility Index (VIX) has not closed below 15 since early October. Investor concerns mostly center around the depth of a prospective global economic slowdown which has taken root in both China and Europe. Recent economic data releases from China have confirmed bears’ fears that the world’s second largest economy is flashing economic warning signs, at the same time European bond markets are forecasting economic growth deceleration on the continent. The yield on the 10-year German bund has fallen back to .21% from 0.57% just two months ago. US economic data has been markedly better than the rest of the world, but weaker than expected corporate reports from FedEx Corp. and Apple Inc. have raised red flags about 2019 growth prospects for U.S. companies that do business overseas. Friday’s blockbuster jobs report put recession bears on their heels but the recent U.S. Manufacturing PMI report, which is forward looking, suggested rockier times may be ahead for the U.S. economy.

Research analysts have been slow to incorporate a cooler economy into their 2019 forecasts but are starting to adjust. The consensus bottoms up forecast for 2019 S&P 500 earnings per share now stands at $172.53 according to data from FactSet, down from $177 at the beginning of 4Q18. As companies report 4Q18 results in the coming weeks and issue new forward guidance, expectations could fall further. Our CJL view is that the S&P 500 will produce $170 in earnings per share this year, representing a 5.7% advance from 2018’s expected level. That is a meaningful deceleration from the 2018 tax-cut fueled growth rate for 2018 index earnings, which are now expected to be up 22% year-over-year. But it is consistent with prior years’ growth rates which were marked by slow and steady economic and profit growth. In fact, S&P 500 earnings per share grew by 6.4%, 4.8%, and 6.6% in 2012, 2013, and 2014 respectively and the cumulative return on the index for that period was 74.6%, with a 20.4% compound annual growth rate. The challenge for stocks, however, may not be the level of forecasted earnings growth but the magnitude of the deceleration. The market looks to be trying to calibrate the downshift and is struggling to find the right valuation to apply to the lower level of earnings growth.

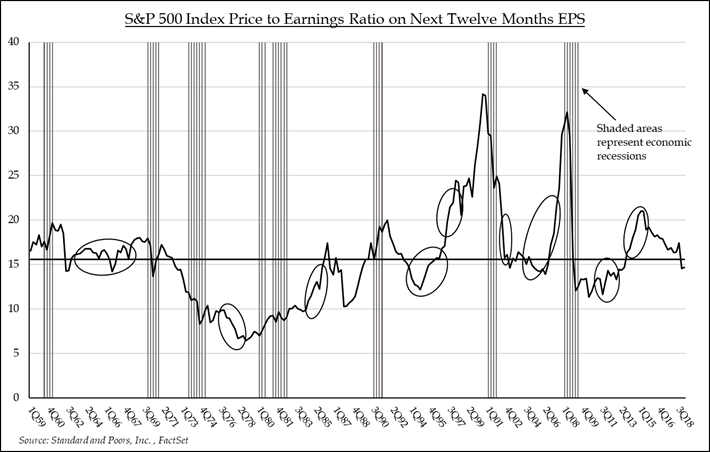

S&P 500 Index Price to Earnings Ratio on Next Twelve Months EPS

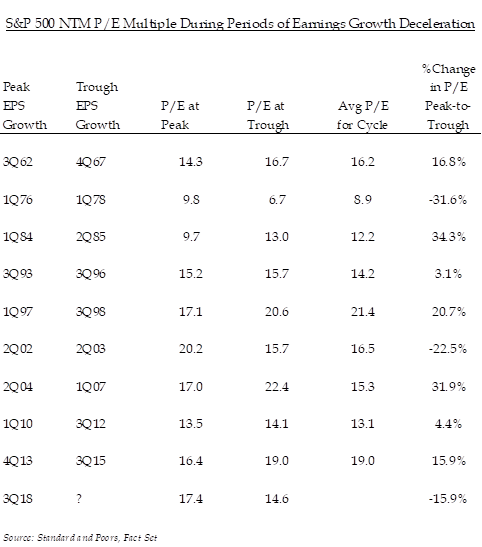

Conventional wisdom is that the market multiple (the P/E on the S&P 500) compresses during times of decelerating earnings growth and expands in advance of accelerating earnings growth. But the results differ depending on whether the deceleration culminates in a recession. Our analysis suggests there have been nine periods since 1960 when earnings decelerated for more than a three-quarter cycle not ending in a recession. The average P/E multiple on next-twelve-months earnings for the S&P 500 during those periods was 15.2x, which is near the long- term average of 15.8x. In seven of the nine periods, the multiple actually expanded between peak earnings growth and trough earnings growth. Of the two periods experiencing multiple compression, the 1976 to 1978 period stands out as one ravaged by rampant inflation which eroded purchasing power and stock valuations. Using 3Q18 as the current cycle peak in quarterly earnings growth, the S&P 500 NTM P/E multiple has compressed by 16% and now stands at 14.6x. Given the likelihood of future earnings forecast reductions, it is difficult to make the case for multiple expansion, despite historic precedence. But the odds favor a bottoming process for the market multiple around the 15x level. Applying a 15x multiple to our $170 earnings forecast would generate a fair value for the index of 2,550, only slightly higher than the current price. If our estimates hold, 2019 is likely to be a low-return year for stocks, putting added emphasis on active managers and investors to find sectors and stocks that can generate sales, earnings, and returns in excess of the broader markets. Attractive prospects for outperformance can be found in the technology, health care, and communications services sectors and we remain overweight in all three.

S&P 500 NTM P/E Multiple During Periods of Earnings Growth Deceleration | Source: Standard and Poors, FactSet

Terry Gardner Jr. is Portfolio Strategist and Investment Advisor at C.J. Lawrence. Contact him at tgardner@cjlawrence.com or by telephone at 212-888-6403.