- January 14, 2019

- Blog , The Portfolio Strategist - Terry Gardner

C.J. Lawrence Weekly – Individual Investors Sell Stock and Bond Funds, While Institutional Investors Shun Stocks

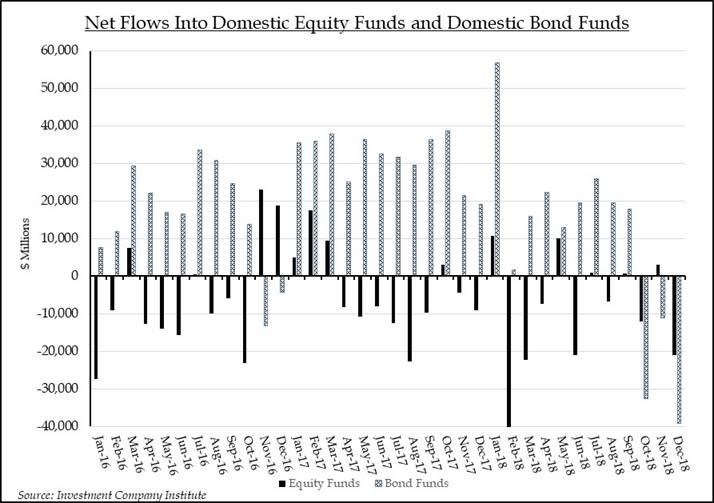

Outflows from domestic equity mutual funds and exchange traded funds (ETFs) accelerated into year-end 2018. According to data from the Investment Company Institute (ICI), domestic equity funds experienced outflows of $105.5 billion in 2018, $30 billion of which flowed out in the fourth quarter. The year-end outflows mirrored the growing negative sentiment that culminated in a meaningful December stock price downdraft. The American Association of Individual Investors sentiment survey recorded a 50% bearish reading at the end of 2018, near survey highs, and well above the long-term bearish average of 30%. The spike in bearish sentiment proved to be a good BUY signal for contrarian traders as the S&P 500 regained 3.6% in the first two weeks of the new year.

Net Flows Into Domestic Equity Funds and Domestic Bond Funds | Source: Investment Company Institute

The recent ICI report also highlighted an unusual occurrence for bond funds. After 21 consecutive months of inflows into bond funds, bond mutual and exchange traded funds experienced outflows in October, November, and December. In fact, the outflows from bond funds were greater than the outflows from stock funds during this period. The relative fund flow trend continued into the beginning of the new year with some fund tracking services suggesting that stock funds are currently experiencing inflows while bond fund flows remain mixed. The last time a shift in favor of stock funds occurred was during the last two months of 2016, after the Presidential election, as investors shifted allocations away from bond funds and into stock funds based on expectations of new business and market friendly policies from the incoming Administration. The end of 2018 was different in that both asset classes saw meaningful outflows, reflecting broader concern for both the economy and financial markets.

Institutional investors are also indicating that that their appetite for stocks is waning. A recently released survey conducted by BlackRock of 230 global institutions, managing $7 trillion in assets, suggested that over half of the participants plan to decrease their allocation to equities in 2019, up from 35% in 2018’s survey. That figure rises to 68% when measuring investors in the United States and Canada. The beneficiary of equity asset class disfavor looks to be private equity. 48% of the survey’s participants intend to increase their allocation to that asset class in the coming year. Despite a slow-down in private equity fund raising in 2018, on the back of a record year in 2017, $426 billion in new funds was raised. A recent Deloitte study suggests that there is now over $1.0 trillion in private equity funds ready to be deployed, regardless of credit conditions. Flush with cash and facing a shortage of private targets, private equity funds may have to re-consider public-to-private transactions, which are at a decade low in terms of deal volume and may represent the only targets on the range.

Terry Gardner Jr. is Portfolio Strategist and Investment Advisor at C.J. Lawrence. Contact him at tgardner@cjlawrence.com or by telephone at 212-888-6403.