- December 28, 2017

- Blog , The Trusted Navigator - Bernhard Koepp

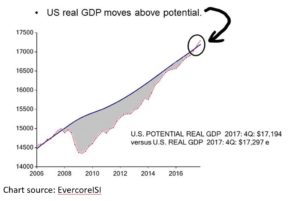

“US GDP Moves Above Potential” – Implications for Markets

Using Reinhart and Rogoff’s work, suggesting that it normally takes a decade for an economy to reach potential output growth following a financial crisis, our former CJL colleague, Ed Hyman, at Evercore ISI points out that the US economy has finally broken out of its decade of sub-par growth (see chart), and is entering a “new decade” of growth. This has profound implications for investors. Clearly “animal spirits” are back and businesses have been incentivized under the new tax regime to deploy capital and invest in their businesses. Under the new tax bill, corporations can expense at a 35% rate, and book profits at a 21% tax rate. That should spur an investment boom leading to accelerating productivity, especially if coupled with foreign cash repatriation. Today’s Chicago Purchasing Managers Index (an index measuring the health of the US manufacturing sector) came in at 67.6 for December (consensus was 62.0), the highest reading for the year. The January 2017 reading was only 50.3! The economy is clearly on the move, but capacity utilization is still 2.8% below the long-term average (since 1972) of 80%.

Using Reinhart and Rogoff’s work, suggesting that it normally takes a decade for an economy to reach potential output growth following a financial crisis, our former CJL colleague, Ed Hyman, at Evercore ISI points out that the US economy has finally broken out of its decade of sub-par growth (see chart), and is entering a “new decade” of growth. This has profound implications for investors. Clearly “animal spirits” are back and businesses have been incentivized under the new tax regime to deploy capital and invest in their businesses. Under the new tax bill, corporations can expense at a 35% rate, and book profits at a 21% tax rate. That should spur an investment boom leading to accelerating productivity, especially if coupled with foreign cash repatriation. Today’s Chicago Purchasing Managers Index (an index measuring the health of the US manufacturing sector) came in at 67.6 for December (consensus was 62.0), the highest reading for the year. The January 2017 reading was only 50.3! The economy is clearly on the move, but capacity utilization is still 2.8% below the long-term average (since 1972) of 80%.

The new Federal Reserve Board, led by Jerome Powell, will be paying close attention to this, given rates are still abnormally low. It also means the unemployment rate should continue to decline, and the lack of supply of labor and the rising participation rate should lead to higher wages. This is all very bullish for an economy that is led by consumption. There are still very few economists using a 2018 GDP estimate above 3%. That may change. Our outlook at C.J. Lawrence is that we should continue to see a normalization of economic conditions in 2018 and another good year for stocks.

BK

12/28/17

Full Disclosure: Nothing on this site should be considered advice, research or an invitation to buy or sell securities, refer to terms and conditions page for a full disclaimer.