- December 20, 2017

- Blog , The Trusted Navigator - Bernhard Koepp

“A Perfect Year” – Outlook for 2018

As of this writing, 2017 is the first perfect year where the S&P500 had a positive return every month for the entire year. 2017 also coincides with the US Output Gap swinging back to the long-term trend line which we haven’t seen for a decade meaning that the economy is back on track. Economies around the World are in a synchronized upswing and populist pro-business, anti-tax & regulation politicians are challenging establishment politics everywhere. Meanwhile, Central Banks around the world are still slow to exit highly accommodative monetary policies.

At my recent visit to my local barber shop customers were debating the merits of the latest rise in bitcoins and if it is a good time to get in. My friends in the art world are still trying to explain how a questionable, poorly restored DaVinci painting could sell for $450 million, more than double the latest record set by a prominent Picasso. The public is starting to pay attention to the stock market and rising asset prices. The world is clearly awash in money and excess liquidity.

As a market practitioner since the late 1980s, 2017 feels much like the mid-nineties when markets continued to move up despite plenty of pessimism and cautionary advice from strategists and policy makers. In fact, 1995 was the last near perfect year and was followed by a few more years of 20%plus returns. The key difference to the late nineties is the absence of inflation in the current cycle. If bonds, the largest global assets class, do not offer competitive yields, stocks will continue to be the only game in town. It is not lost on portfolio managers that exceptional years are often followed by higher returns, because asset allocators are often slow to adjust to new conditions.

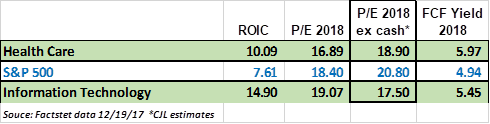

At C.J. Lawrence, where we manage portfolios for private clients, we try not to get too caught up in the macro debate but continue to find value in traditional growth sectors: Technology and Healthcare. Both of these sectors’ P/E ratios based on 2018 estimates trade at no premium excluding cash to the S&P500 while defensive sectors like Utilities and Consumer Staples sell at a premium to the market on the same measure. This should be in reverse. Free cash flow yields and returns on invested capital (ROIC) are also significantly higher for technology and healthcare stocks.

Among our core Technology holdings, we are confident that much of the future revenue growth driven by innovation will be captured by the larger companies. These fierce competitors, which we call “Bulldogs” at C.J. Lawrence (Google, Facebook, Microsoft, Intel, Amazon) are investing heavily in machine learning or what is known as artificial intelligence (AI). AI will drive the next leg of growth in the economy building on the head start these companies already enjoy in cloud computing. The barriers to entry in AI are high for new companies because they don’t have access to the large pools of data that have been accumulated by these dominant companies. New entrants also lack the human resources to exploit this new opportunity. Innovations in Technology are also a reason we remain optimistic about the healthcare sector where “Big Data” is a disruptor in how we administer and distribute traditional healthcare. The intersection of cheap computing power and the advent of human genome sequencing are creating new competitors on the diagnostics side which are the new emerging growth stocks of the next decade. This has drawn the attentions of the likes of Amazon which is applying to become a distributor of healthcare products and services, and Apple whose suite of wearable devices are increasingly geared towards personal health.

There is no doubt that there is plenty of optimism going into 2018, not only among market practitioners but also increasingly among the investing public. Retail investors have been largely on the sidelines during the ‘great recovery’ in stock prices off the 2009 low. In fact, inflows into bonds have trumped inflows into stocks by a wide margin in the last decade. History teaches us to be vigilant at this point in the cycle but also not too cautious. We believe 2018 could be another good year for the patient investor.

BK

12/20/17

Full Disclosure: Nothing on this site should be considered advice, research or an invitation to buy or sell securities, refer to terms and conditions page for a full disclaimer.