- September 24, 2022

- CJ Lawrence , Market Commentary , The Trusted Navigator - Bernhard Koepp

Relative Strength Indicator (RSI) Back to Extreme Oversold Condition – C.J. Lawrence Market Commentary – 9/23/2022

It has been a tough couple of weeks for the bulls. The S&P500 is back to the June low at 3693, wiping out the strong momentum we saw in August and back to extreme oversold conditions as measured by the relative strength indicator (RSI). The culprit is core inflation or what is often called PCE (personal consumption expenditures), a cleaner reading of inflation as compared to CPI, excluding food and energy prices. Prices paid by consumers for goods and services remain stubbornly high despite headline inflation (CPI) coming down sequentially for the last three months.

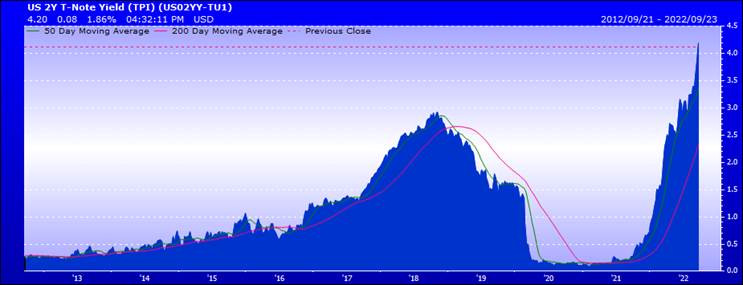

Jay Powell’s Fed continued to raise rates aggressively with the latest 3rd consecutive increase of 0.75%. The Fed Funds rate now stands at 3.25%, which was not surprising. The Fed’s dot-plot for Fed Funds showed a much higher terminal rate at 4.5%, which spooked the market and set off another round of selling in stocks and bonds. By the end of the week, the 2-yr Treasury yield surged to 4.2%, a level not seen in a decade, see chart below. The interest rate for 30-year fixed mortgages is now near 7%, and housing, including rents, is rising from very high levels. Higher short-term interest rates are now offering savers some relief if you are looking to hide in cash.

We continue to stick to our view that inflation will trend down in the coming months, perhaps even significantly. We look to our former colleague and top-ranked economist, Ed Hyman who noted that the recent reading of core inflation may be an outlier and that lower commodity prices will continue to bleed into a lower PCE. Our more constructive view on equities near-term is highly dependent on inflation coming down. So far, we have been wrong on the speed of that decline. The Fed’s more hawkish stance regarding raising interest rates raises the risk of financial dislocations, i.e. something may break in the global economy. The probability of a soft landing is now more unlikely. With that in mind, we are watching currencies very closely. The US Dollar is breaking out, and we are effectively exporting inflation to the rest of the world. A breaking point is more likely to come from abroad, given our domestic banking system is well capitalized and consumer balance sheets still look healthy. Europe is one of the areas to watch, given parts are already in a recession.

One of my close friends in the business recently asked me, “What would make you bearish?” A fair question for a portfolio manager who believes investing, by definition, is a positive endeavor. I would become bearish if I did not believe inflation could get back to a level closer to 3-4%. That may seem optimistic from current levels, but businesses are reacting rapidly to changing conditions. A key driver of that change is technology, which drives about 40% of our economic growth today.

The problem with inflation is that it is on the supply side. Destroying demand by increasing interest rates won’t be enough. The good news is we are seeing global supply chains easing, and business managers are adapting to a post-pandemic economy where labor is structurally scarce. It may take a bit more time for markets to price in these changes and the uncertainty associated with them, but we may be getting closer to that point. We, therefore, remain optimistic that the current oversold conditions may offer another interesting entry point for patient investors.

Bernhard Koepp is CEO and Portfolio Manager at C.J. Lawrence. Contact him a bkoepp@cjlawrence.com by telephone at 212-888-6342.