- November 18, 2019

- Blog , The Portfolio Strategist - Terry Gardner

C.J. Lawrence Weekly – U.S. Manufacturing Economy Not Yet Ready to Turn

With the U.S. consumer carrying much of the water for the U.S. and global economies, the market continues to wait for some support from manufacturing. But, to date, the manufacturing cavalry does not look ready to ride. While much of the recent slowdown in U.S. manufacturing can be blamed on the UAW national strike of General Motors, U.S. manufacturing activity was declining prior to the strike and continues to be challenged. The trade battle between the U.S. and China, and slow consumption growth in Europe are more likely to be taking their toll than the strike. Excluding the 7.1% drop in motor vehicle output, which was the largest decline since January, October factory production decreased 0.1% for a second month, according to Federal Reserve data. Total industrial production, which also includes output at mines and utilities, slumped 0.8% in October, the largest decline since May 2018.

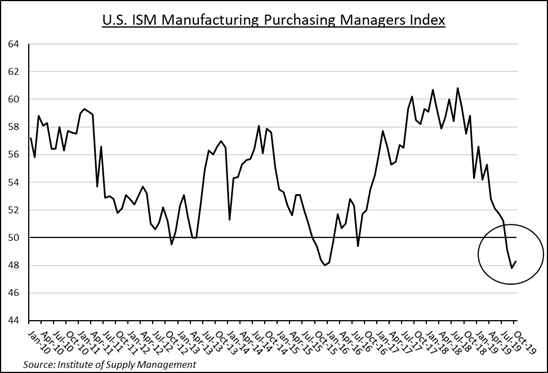

The Institute for Supply Management’s gauge of activity has contracted for three consecutive months, while a separate index showed global manufacturing shrank in October for a sixth consecutive month. U.S. manufacturing capacity utilization, which measures manufacturing plant utilization, came in at 74.7%, the weakest reading since September 2017. Manufacturing, which makes up about three-fourths of total industrial production, accounts for about 11% of the U.S. economy.

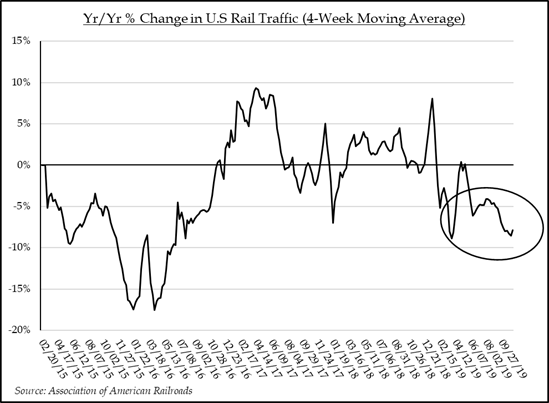

Other leading indicators suggest that a manufacturing recovery is not imminent. Rail shipments offer a view into future economic activity as their cargo fuels the supply chain of output and finished goods. That data continues to be soft with last week’s release showing further declines. Intermodal (transportation of shipping containers on rail cars) loadings show similar deterioration. Even the Baltic Dry Index, which acts a good barometer for global shipping demand for dry bulk commodities, has fallen from its recent peak notwithstanding reduced ship capacity driven by new emissions restrictions. Despite the weakness in the underlying freight economy, analysts who track industrial and materials companies remain optimistic. Earnings per share for the S&P Industrials Sector Index and S&P Materials Sector Index are forecasted to grow 17% and 15% respectively in 2020. Investors like their prospects and have bid the respective index prices up 28% and 19.5% year-to-date. Air cargo volumes and buoyant truck tonnage index results may be indicating that a bottoming process is underway. Should a manufacturing recovery materialize, industrial and material sector forecasts could move meaningfully higher.

Terry Gardner Jr. is Portfolio Strategist and Investment Advisor at C.J. Lawrence. Contact him at tgardner@cjlawrence.com or by telephone at 212-888-6403.