- September 16, 2019

- Blog , The Portfolio Strategist - Terry Gardner

C.J. Lawrence Weekly – Rotation to Value Looks Unsustainable

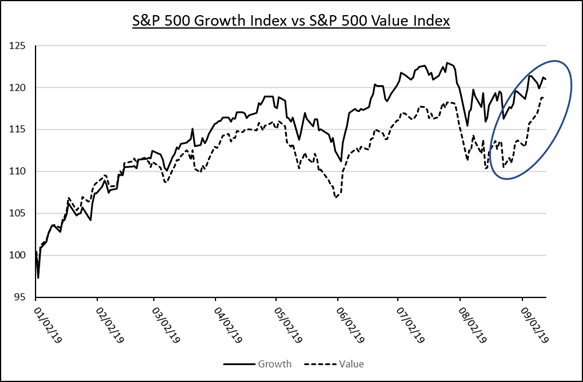

The S&P 500 broke back above 3,000 last week and is zeroing in on its prior peak of 3,026 set back in July. All major S&P sectors are generating positive returns on a year-to-date basis. Technology is still leading the performance pack for the year, followed closely by the bond-proxy REIT sector, and Communications Services. But as the market has pushed higher during the past two weeks, leadership shifted, and perennial favorites faltered. Last week the top performing sectors included value-oriented Financials, Energy, and Materials, while Technology and REITs were among the worst performers. The internal shifts have market watchers asking if value style investing has come back into favor. We think the economic environment continues to favor growth and that the recent rotation is more technically driven than fundamentally inspired.

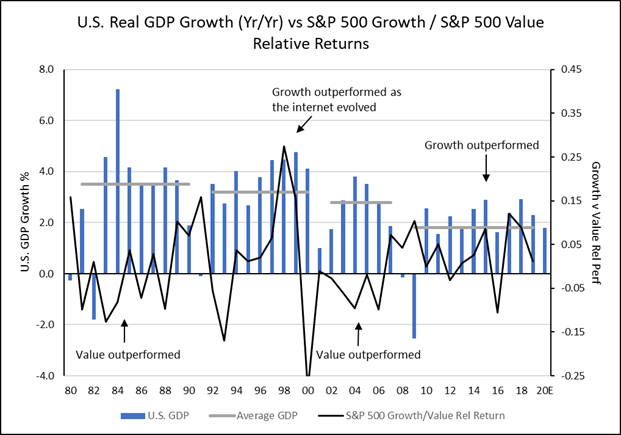

While practitioner definitions of “value” and “growth” vary, there is consensus that value stocks are categorized as such by their relative low valuations on sales and earnings and on their sensitivity to cyclical elements of the economy. As such, value stocks have typically delivered relative outperformance when the economy is inflecting and moving towards higher rates of growth. The thesis holds that constituent companies will benefit the most from a robust economy and that their stocks can be purchased at attractive valuations relative to the rest of the market. Conversely, growth stocks tend to outperform when their prospects for sales and earnings growth outshine the growth profiles of companies more reliant on macro conditions for a lift. This relationship has remained intact for decades, except for the period in the mid-1990s when growth stocks outperformed on the back of the evolution of the internet and the e-commerce business landscape. Growth has largely outpaced value for the entirety of the current economic expansion which has been noted for its shallow rate of annual growth.

For the status quo to be upended the U.S. economy would likely need to expand at a greater-than-average rate and give lift to cyclical company profitability. But, at present, the economy looks to be heading in the opposite direction. The U.S. consumer remains the bright spot in the GDP growth equation (accounting for 2/3 of US GDP output) but government and corporate spending appear to have run out of gas, and international trade is waning. That is not a constructive backdrop for robust GDP growth, and for cyclically sensitive stocks. But the recent resurgence in long-dated U.S. treasury bond yields has unleashed technical forces that systematically shifted allocations from appreciated growth stocks to unloved value names. The U.S. 10-year treasury benchmark yield climbed from 1.5% before Labor Day to over 1.9% last week! The re-allocation may continue for a period but looks unsustainable to us based on fundamentals. We continue to favor stocks of growth companies that drive their own fate and grow market share regardless of economic conditions.

Terry Gardner Jr. is Portfolio Strategist and Investment Advisor at C.J. Lawrence. Contact him at tgardner@cjlawrence.com or by telephone at 212-888-6403.