- December 10, 2018

- Blog , The Portfolio Strategist - Terry Gardner

C.J. Lawrence Weekly – Overweight Communications Services Sector for Both Offense and Defense

The stock market’s recent swings have been dramatic. On several occasions the S&P 500 has completed a round-trip move of more than 3% in a single session. Last week the Index reached a high of 2,800 but finished the week at 2,623, down 6.3% from the intra-week high and down 4.6% for the week. The market’s price action highlights its fragility and investor and trader lack of conviction in directional moves. Tweets, headlines, and rumors are giving the markets fits at a time when longer-term investors are grappling with the prospects for slowing global growth. But while the broader market has been unpredictable, patterns within the market have been quite consistent. On big equity decline days, treasury bond prices have rallied and equity investors have rotated to “defensive” sectors like utilities, real estate, and consumer staples, and out of stocks that have outsized year-to-date gains or meaningful overseas sales exposure. Technology shares have suffered the largest declines as they meet both criteria.

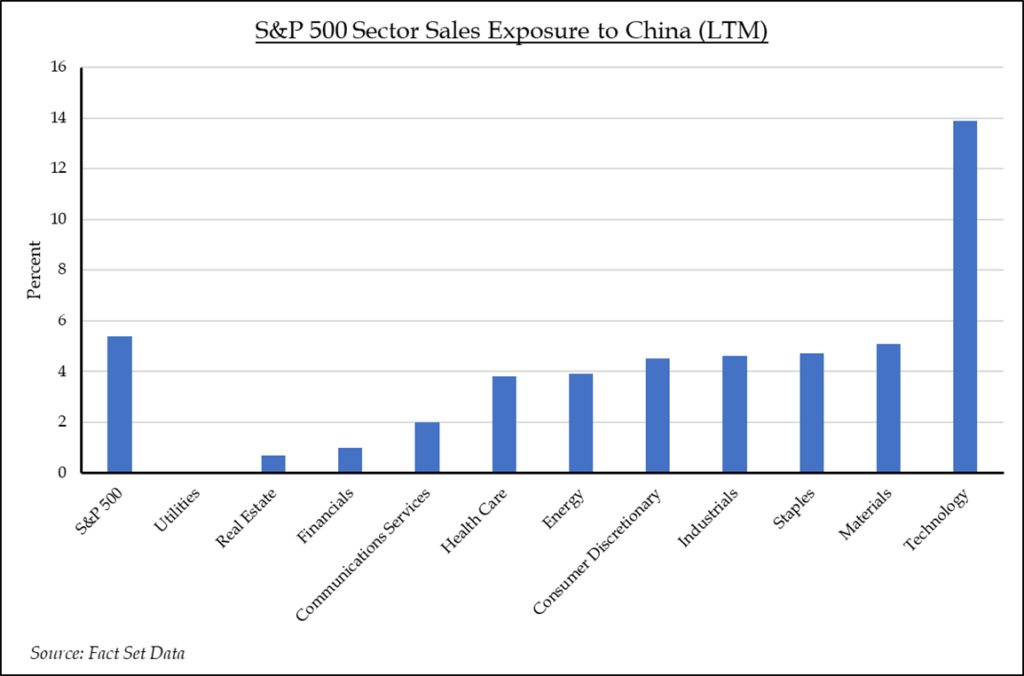

The two areas of macro focus for most stock investors continue to be the status of trade with China and the outlook for profit margins in the face of growing wage pressures at home. Thus, the attractiveness of utilities and real estate investment trusts has grown beyond their defensive characteristics as a result of their predominantly domestic revenue exposure. Consumer staples stocks still check the defensive box due to the resiliency of their revenue streams, but their risks are rising as sector constituents have relatively high exposure to overseas markets. A challenge for investors looking to utilize these sectors in defensive strategies is that they’ve also become expensive. Utilities stocks and real estate investment trusts are trading close to peak historic valuations on a price-to-earnings (P/E) and a price-to-funds from operations (P/FFO) basis. Staples stocks have come off their peak valuations recently but slowing global growth presents major revenue headwinds for most of the sector’s constituents.

S&P 500 Sector Sales Exposure to China (LTM) | Source: FactSet Data

Meanwhile, one sector that has been beaten down over the last year despite a good mix of both defensive and offensive characteristics is the recently created Communications Services Sector. It was formed this fall by S&P Global as part of their GICS (global industry classification system) sector reclassification. The sector carries close to a 10% weight within the broader S&P 500 but still lags that weight in most index funds and ETFs. For instance, the assets under management (AUM) in the Technology Select Sector SPDR ETF is near $19.3 billion, while the AUM in the Communication Services Select SPDR ETF is $3.2 billion. That is close to a 6 to 1 ratio in assets, while the weights within the S&P 500 Index have a 2 to 1 ratio. The imbalance would suggest that sector funds will need to build positions in the Communications Services sector stocks in the coming year to restore relative balances and avoid tracking error. With faster sales growth than the S&P 500, high profit margins, and low international revenue exposure, particularly to China, the sector also looks attractive on both a fundamental and a relative macro basis. To be sure, the sector’s heavy weights, Alphabet and Facebook, continue to face regulatory scrutiny, but both companies’ stocks have been commensurately punished over the past year and are trading at historically low valuations. The sector’s other large industry weights are in the media and entertainment industry groups, which tend to be resilient to economic downturns and are less exposed to wage pressures due to their low compensation cost ratios. Meanwhile Communications Services is the second worst performing sector year-to-date, down ~9.5%. It may have already taken its medicine and is poised for relative outperformance.

Terry Gardner Jr. is Portfolio Strategist and Investment Advisor at C.J. Lawrence. Contact him at tgardner@cjlawrence.com or by telephone at 212-888-6403.