- June 25, 2018

- Blog , The Portfolio Strategist - Terry Gardner

C.J. Lawrence Weekly – Down but Not Out…Industrial Stocks Warrant a Closer Look

Investors in industrial stocks are likely disappointed with the sector’s year-to-date price performance. The S&P Industrials Sector Index price is down 4.3% year-to-date despite being up 5.1% over the last year. The sector became a market darling in late 2017, but lost its luster in early 2018 as fears of international trade battles percolated. According to FactSet data, over 36% of sector revenues come from outside the U.S. Adding to industrial stock owners’ anxiety is a comment made by Caterpillar’s (CAT) management during their 1Q18 earnings call, which they have since retracted, suggesting that the current economic environment could be as good as it gets. That comment, as off-the-cuff as it sounded, stoked investor fears that sector earnings were approaching a cyclical peak, and catalyzed a re-rating of industrial shares. The sector is now down over 9% from its January high. But a closer look at sector fundamentals, and the progression of sales and earnings forecasts, suggests that industrial stocks may have been prematurely discounted.

In early 2018, analysts recalibrated earnings forecasts to incorporate the impact of corporate tax reform. Prior to the adjustment, the 2018 earnings per share forecast for the S&P Industrials Sector Index was $32.73. By the end of March, the tax reform-adjusted estimate was $36.00. On average, analysts expected that tax reform would increase annual earnings per share by ~10%. That was a healthy boost to earnings that were already expected to grow by 9.4% from 2017 levels. Sector earnings per share are now projected to grow 18.6%, 12.7%, and 11.7% for 2018, 2019, and 2020 respectively. Bears have seized upon the downward slope of the growth curve, suggesting that earnings growth has peaked and that the group therefore deserves a lower price-earnings (P/E) multiple. But stripping out the tax reform adjustments paints a different picture. By our estimates, the pre-tax reform, organic growth progression looks more like 7.5%, 11.9%, and 11.7% in 2018, 2019, and 2020, respectively. That is an attractive earnings growth profile for a sector now trading at a forward earnings multiple below its’ 15-year average. Sector revenue growth is expected to jump 8.2% this year, off-setting low levels of domestic capital spending and sales growth between 2014 and 2016. Top-line growth is expected to resume a steady pace in 2019 and 2020 with estimates forecasting 5.5% and 5.7% advances.

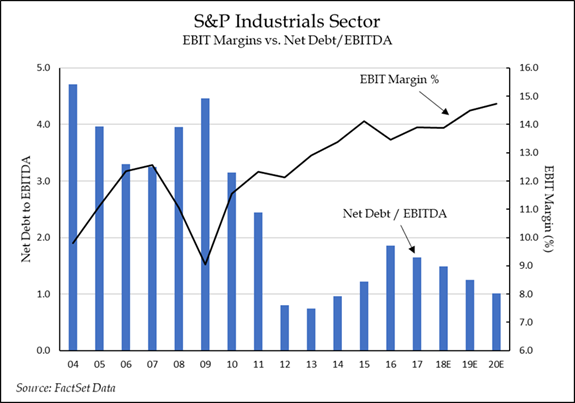

S&P Industrials Sector – EBIT Margins vs Net Debt/EBITDA

To our eye, the out-year sales and earnings forecasts look conservative. The current economic backdrop remains constructive, oil and natural gas prices have rebounded to the point of spurring capital investment, and general capital expenditure growth is accelerating. Additionally, should a badly needed national infrastructure plan come together in the next 12-24 months, industrial companies would be the direct beneficiaries. Furthermore, the Index’s constituents look to have learned hard lessons from the past financial crisis and subsequent recession. Leverage ratios are near cyclical lows while EBIT margins are at historic highs. The increased business model leverage positions industrial companies to weather trade related disruption should it materialize, and to ramp faster earnings growth in a stable and/or improving economic environment. Trade related risks to the broader market look to be increasing, and industrial stocks are not immune to trade war related disruption. But industrial stock prices may already reflect much of that risk and may not be discounting the possibility that we are in the midst of a capital spending cycle that is supportive of multi-year earnings growth. It may be a bumpy path forward, but industrial stocks warrant another look.

Full Disclosure: Nothing on this site should be considered advice, research or an invitation to buy or sell securities, refer to terms and conditions page for a full disclaimer.