- May 6, 2019

- Blog , The Portfolio Strategist - Terry Gardner

C.J. Lawrence Weekly – Labor Productivity Leadership Should Be Embraced

Last week’s U.S. Labor Department report stated that U.S non-farm labor productivity rose at a 3.6% annualized rate in the first quarter of 2019. That was welcome news for stock market bulls who had been viewing the lack of worker productivity as an obstacle to growth, or as a path to higher unit labor costs and inflation. Indeed, the fastest pace of worker productivity improvement in four years was accompanied by only a 0.1% rise in unit labor costs, the weakest result since the fourth quarter of 2013. The combination of 3.2% GDP growth and tepid inflation has created a favorable backdrop for stock prices.

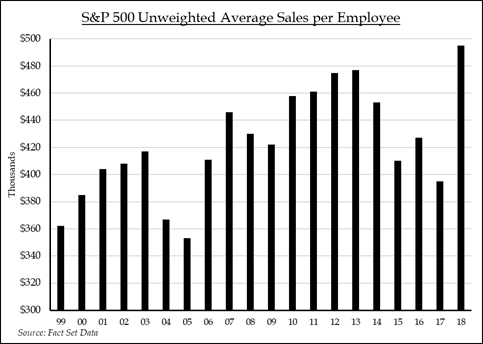

Many economists challenge the methodology used to calculate labor productivity and whether the Labor Department’s metrics are suitable for the modern economy. But recent reports match up well with trends in S&P 500 Index constituent sales-per-employee measurements. In fact, S&P 500 companies may lead the broader economy in productivity reporting, as 2018 showed strong improvement in sales-per-employee, well ahead of last week’s encouraging productivity report. With headline unemployment now at 3.6%, companies are struggling to find qualified workers and are seeking ways to do more with less. Many are managing success through automation and other productivity initiatives. Indeed, despite the tight labor market, top line growth for the index is forecasted at 5.0% in 2019 and 5.3% in 2020. Inflation is expected to remain subdued with employee counts forecasted to remain close to current levels. That would suggest that labor productivity will likely play a meaningful role in top line growth.

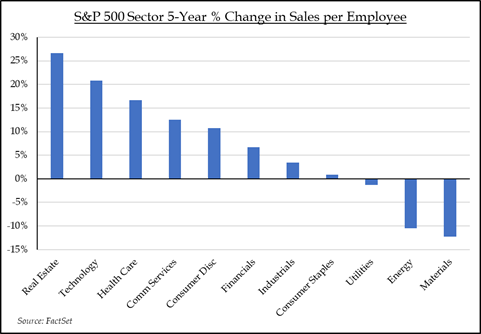

Among the sectors experiencing the largest increases in employee productivity over the past five years, Real Estate, Technology, and Health Care have been leaders. Real Estate is unique in that it is not an employee-heavy sector. The sector’s constituents have instead benefitted from a 30+% increase in net revenue driven by higher property sales and prices across all segments. Meanwhile Technology companies have been eating their own cooking and finding ways to enhance employee efficiency and productivity through robotics, automation, and new software. Capital spending by technology companies has increased over 10% each year for the past three years, increasing the likelihood that productivity trends will continue. Meanwhile, with the specter of lower drug and product prices looming, Health Care companies are also finding ways to improve the productivity of their work forces. As health care margins come under increased pressure, health care managements will be hard at work exploring worker productivity investments that can help drive higher unit sales. A common theme among the leaders is their use of technology to enhance worker productivity and drive top line growth. These leaders are at the forefront of innovation and productivity warranting increased investor attention in any market environment.

Terry Gardner Jr. is Portfolio Strategist and Investment Advisor at C.J. Lawrence. Contact him at tgardner@cjlawrence.com or by telephone at 212-888-6403.