- April 29, 2019

- Blog , The Portfolio Strategist - Terry Gardner

C.J. Lawrence Weekly – U.S. Capital Spending Growth Looks Poised to Reaccelerate

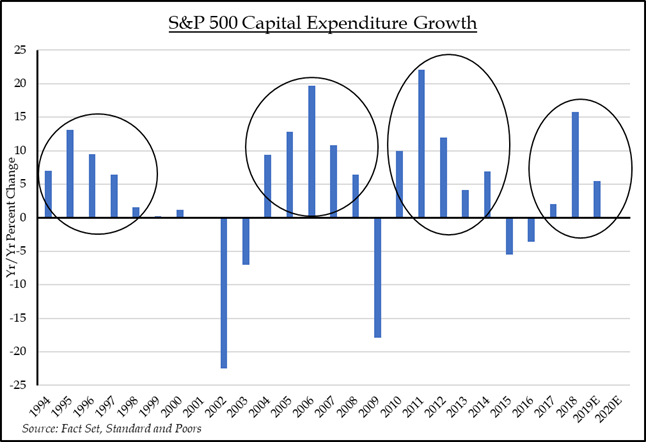

When the Tax Cut and Jobs Act passed in December 2017 the consensus expectation was that lower corporate income tax rates, lower tax rates on repatriated overseas capital, and increased incentives for near-term capital investment would spur a durable capital spending cycle in the U.S. Indeed, capital expenditures (capex) among S&P 500 Index constituents rose 16% in 2018, according to data from FactSet. But trade uncertainties and increased prospects for slowing global economic growth put a pause on corporate spending intentions late in 2018. Analysts reacted by lowering 2019 S&P 500 annual capex spending forecasts to 5.5%, which remains slightly ahead of the 25- year annual average of 4.5% and lowered the 2020 estimate to 0%.

Last month’s durable goods orders report may be signaling that capex estimates have fallen too far, and that higher levels of spending are sustainable. The March report from the U.S. Commerce Department stated that orders for non-defense capital goods, excluding aircraft, a closely watched proxy for business spending plans, surged 1.3% in the month, to an all-time high of $70,0 billion. The jump accounted for the biggest increase since last July and followed a 0.1% gain in February. The increase was fueled by a pick-up in demand for computers and electronic products. Meanwhile, energy company spending which has declined for five straight months as independent producers follow through on plans to cut spending on new drilling and completions, may reverse itself in the coming months as super-major energy companies turn their focus to the Permian and surrounding basins to increase oil and gas production.

Historically, S&P 500 capital expenditure growth has trended in cycles, with two years of declines followed by five years of growth. S&P 500 Index capex declined in both 2015 and 2016 suggesting that, if history repeats, 2017 through 2022 should be expansion years. Flush corporate balance sheets, combined with aged equipment fleets and trends towards cloud computing, 5G network transformation, and manufacturing automation should all encourage positive capex trends so long as the economy stays on track. Emerging fears of a future roll-back of favorable expensing rules should the political landscape in Washington D.C. shift in the next election cycle, could also encourage near-term spending increases by companies seeking to take advantage of the current tax treatment on capital expenditures. Technology and industrial stocks are the likely beneficiaries of an extended capex cycle, with technology warranting a meaningful overweight in growth portfolios in our view.

Terry Gardner Jr. is Portfolio Strategist and Investment Advisor at C.J. Lawrence. Contact him at tgardner@cjlawrence.com or by telephone at 212-888-6403.