- June 7, 2023

- CJ Lawrence , Market Commentary , The Trusted Navigator - Bernhard Koepp

This Time It’s Different – Bernhard Koepp, C.J. Lawrence – Market Commentary 6/7/2023

Markets are up over 20% since the October 12 low, which typically signals the start of a new bull market. The Nasdaq is up 35% and the Dow Jones Industrial Average is up 15% for the same period, but nobody cares. Sentiment remains bearish. Short interest remains high and if you followed the talking heads on your favorite financial cable channel or blog, most have called the direction and underlying leadership of the market completely wrong. Even our favorite economists are surprised by the underlying resilience of the US economy. Last Friday the US economy reported adding 339,000 jobs in May crushing expectations of 195,000. Workers are returning to the labor force, a bullish sign for the economy, explaining an uptick in the unemployment rate from a historically low 3.5% to 3.7%. Even inflation surprised to the downside. Unit labor cost was down meaningfully, signaling lower inflationary pressures ahead.

When markets turned in October last year we were still in the wake of the global pandemic. Inflation was at a peak at over 9% (CPI). Add to that renewed great power competition not seen since the cold war and you get unprecedented distortions in markets and the global economy which confounds even the smartest prognosticators. It was our sense that, “this time it’s different!”

I covered the banking crisis in detail during my last YouTube at or channel “CJ Lawrence”. We argued that the crisis would signal the end of the current tightening cycle by the Fed. To put the current banking crisis into context, during the great financial crisis of 2008, we initially lost 25 banks and another 400 in the 3 years following. If you remember the Savings and Loans crisis from 1985 to 1995, we lost about a third of our S&L or thrifts, just over 1,000 institutions! What did each crisis have in common? They were followed by good equity markets.

There was a lot of hand wringing about the debt ceiling. Credit agencies like Fitch put US sovereign debt on credit watch. Is this a rerun of 2011 when US debt was cut from AAA by Standard & Poors for the first time just days after President Obama signed the deal? Who knows, but Fitch gave a similar warning just days after the deal was signed by President Biden. It stated, while the deal to raise the debt ceiling and cut spending are positive considerations, repeated political standoffs over the federal government’s borrowing limit lowers confidence in governance on fiscal and debt matters. We shall see if politicians heed the warning not to air our nation’s dirty laundry when it comes to paying our obligations.

We were told by pundits that leadership in the markets will be different for the next bull market. As bottom-up, fundamental analysts, we were skeptical of this point of view because Technology, represents a much larger and more predictable portion of the global economy today. The pandemic pulled forward the adoption of cloud computing in the enterprise. This created highly recuring revenue models among many of the very large Tech companies. That puts them in a much more favorable position coming out of the last downturn.

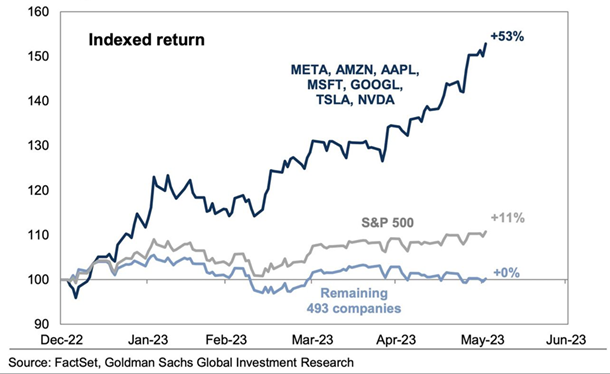

Lastly, we were told that 2023 should be better for stock pickers. As active managers, we welcome such a market, but so far, 2023 has been much like 2022, with very narrow leadership. In 2022 it was a handful of energy stocks that determined outperformance. In 2023 it’s all about 7 mega cap stocks, including Amazon, Apple, Alphabet, Facebook, Microsoft, Nvidia, and Tesla which are up 53% collectively ytd as of June 1st. The rest of the market is flat! (see chart) For the market to continue to go up, we need a broadening of stock and sector performance beyond this narrow group. We believe that may happen once the macro-economic picture for the more cyclical portion of the market (Financials, Industrials, Consumer) becomes clearer.

Bernhard Koepp is CEO and Portfolio Manager at C.J. Lawrence. Contact him a bkoepp@cjlawrence.com by telephone at 212-888-6342.