- April 7, 2022

- Blog , The Trusted Navigator - Bernhard Koepp

Markets Bottomed in Q1 When Oil Peaked

This post was originally written on April 1, 2022, 5:45 PM EST.

The first quarter of 2022 finished yesterday with the S&P500 down 4.9%, the Tech-heavy Nasdaq down 9.1%, and the Dow Industrials down 4.6%. Oil prices peaked on March 8th at $128 per barrel (Brent crude oil) and the market bottomed around that same time, clawing back about half of the loss incurred for the quarter. Most of the damage to Technology stocks actually happened well prior to the Ukraine war, as these typically higher valuation growth stocks already adjusted to the probability of higher interest rates and inflation. Prudent positioning going into the current interest rate cycle was to be overweight banks, which could benefit from higher interest rates and better economic activity. Adding select industrial or “value” exposure was also the strategists’ favorite given improving macro conditions as we exit the global pandemic.

That market playbook was flipped on its head with the uncertainties of the Ukraine war which began on February 24th, making it one of the more complex investment environments we have seen, even for our veteran team of portfolio managers! Bank stocks that outperformed until February 24th reversed course and began to underperform dramatically from the day of the invasion. Financial stocks looked beyond the still highly favorable macro-economic environment, pricing in various recession scenarios, which were non-existent prior to the invasion. The conflict further stoked the already skyrocketing inflation with oil and wheat prices spiking. Important technology components & semiconductors including access to batteries were disrupted and impacted the production of next-generation Electric Vehicles (EVs) and traditional ICE vehicles in an already tightly supplied auto market.

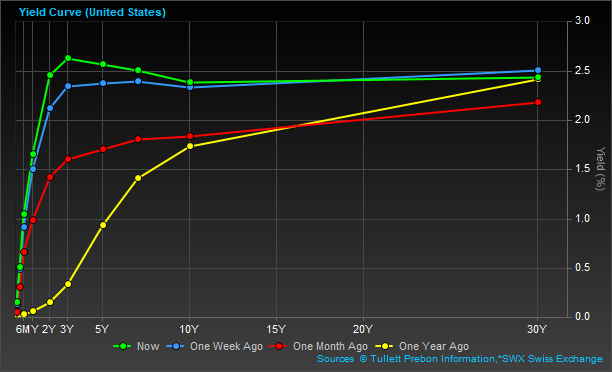

Q1 was a disappointing quarter for most active managers, given that every sector other than Energy and Utilities was down for the quarter. The strength in the March employment data which we saw today as well as the upward revision to the February data points to a solid footing for the US economy. The unemployment rate continues to be on a downward trajectory, now at just 3.6%. The main uncertainty near-term remains the duration of the Ukraine war and the humanitarian crisis unfolding there. It is impressive to see how united the West has become as a result of the conflict which is impacting everything from energy to immigration policies. European economies are bearing the brunt of the oil and gas shock. A recession there is likely. This is already playing out in the relative weakness of the Euro, see chart below. In the US, a recession remains the lower probability scenario despite the now inverted yield curve for maturities from 2yrs to 30yrs, see 2nd chart above.

Bernhard Koepp is CEO and Portfolio Manager at C.J. Lawrence. Contact him a bkoepp@cjlawrence.com by telephone at 212-888-6342.