- September 23, 2019

- Blog , The Portfolio Strategist - Terry Gardner

C.J. Lawrence Weekly – The CJL Rule of 20 Pegs the Stock Market Valuation at Fair Value

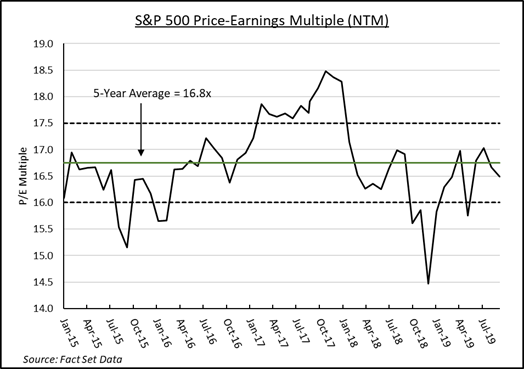

Equity investors demonstrated considerable buying restraint over the past several weeks as interest rates flirted with historic lows. In early September, the U.S. Benchmark 10-Year Treasury Bond yield slipped below 1.5%, where it had not been since 2016 and 2012 before that. Historically, as rates have fallen, investors shifted asset allocations towards equities in search of growth and yield. The result has often been a spike in the S&P 500 price-earnings multiple (market multiple) as equities are re-rated based on waning competition from fixed income securities. But the current multiple on S&P 500 forward earnings remains below its 5-year average and well within the high-low range set during the period.

C.J. Lawrence’s Chairman, Jim Moltz, noted in our recent investment committee meeting that the market multiple looks more closely tethered to inflation than in recent memory. In fact, as interest rates have fluctuated, inflation expectations have been relatively contained. That may account for the lack of volatility in the market multiple. The relationship between price-earnings multiples and inflation is captured in the C.J. Lawrence “Rule of 20” which Jim devised in the 1980s. The Rule suggests that adding the current price-earnings multiple on the S&P 500 to the annual rate of inflation should approximate 20, which is the 50-year historic average of the sum. The calculation has served as a useful measurement tool in analyzing whether the stock market can be considered overvalued, undervalued, or fairly valued. Using a 17x forward multiple on S&P 500 earnings and a 2.3% annual inflation rate generates a Rule of 20 reading of 19.3, which puts the sum in fair value territory.

For most of the current decade the Federal Reserve has struggled to nudge the U.S. economy’s rate of core inflation to, or above, its 2.0% target rate. The current backdrop of low domestic unemployment and slowing international trade looks conducive to higher prices. But record low global interest rates, coincidental global monetary stimulus initiatives, and recovering global GDP growth rates failed to produce any meaningful inflation uptick in the recent past. Perhaps this time will be different, inflation will push higher, and the market multiple will come under some pressure. But for now, the inflation outlook is tame, and the market multiple looks fair. The stock market faces a myriad of risks over the next 12-18 months but our Rule of 20 suggests that valuation is not the loose brick in the wall of worry.

Terry Gardner Jr. is Portfolio Strategist and Investment Advisor at C.J. Lawrence. Contact him at tgardner@cjlawrence.com or by telephone at 212-888-6403.