- September 3, 2019

- Blog , The Portfolio Strategist - Terry Gardner

C.J. Lawrence Weekly – Sales Growers in Communications Services and Healthcare Sectors Have the Right Mix

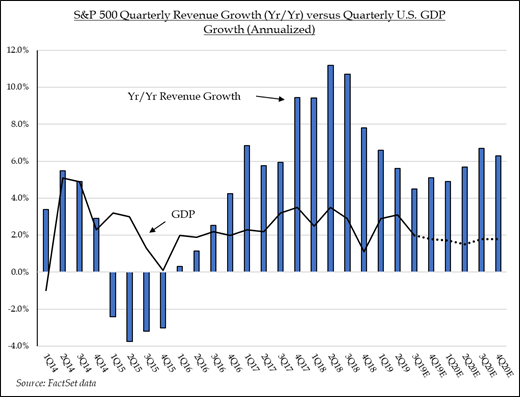

With 2Q19 earnings season mostly in the rear-view mirror, investors and analysts are recalibrating their models to incorporate the recently reported results and refreshed outlook. Despite a slight year-over-year decline in quarterly earnings, S&P 500 earnings per share came in slightly better-than-expected. Top line results showed more resiliency, coming in 4.0% ahead of last year’s level. For the full year 2019, S&P 500 Index sales are now forecasted to increase 4.9% over 2018’s level, while earnings are expected to grow only 2.3% over the same period. The decline in profit margins is expected to be reversed in 2020, according to FactSet bottoms-up estimates.

The rule of thumb for S&P 500 sales is that they typically grow at 2.0-2.5 times the rate of nominal U.S. GDP growth. Consensus GDP forecasts call for 1.9% growth in 2019 and 2.0% growth in 2020, so the 4.9% S&P 500 sales forecast sounds about right. 2020’s S&P 500 sales forecast calls for 5.9% growth, which looks challenging given global economic uncertainty.

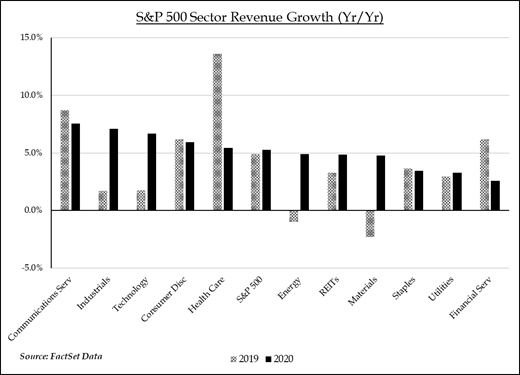

Among the S&P 500 Index sectors, Communications Services, Health Care, and Consumer Discretionary have been delivering impressive sales growth year-to-date and are expected to outpace the S&P 500 again next year. The Technology and Industrials sectors generated GDP-like top line growth in 2019 and their revenue growth is forecasted to reaccelerate in 2020. Meanwhile Materials and Energy sector sales, which have been negative, are also expected to reaccelerate in 2020. But in the mix of sales growers, the Communications Services and Health Care sectors stand out. The bulk of the Communications Services sector is comprised of companies that generate advertising and related transaction revenue, and others that provide entertainment and media services to consumers. Positive attributes include the sector’s high sales exposure to the U.S. consumer, favorable advertising revenue backdrop during political campaign seasons, and recession resiliency of media and entertainment businesses. Meanwhile, despite political overtones that have depressed valuations of most healthcare companies, leading sector constituents are expanding product pipelines, investing in research and development, and have healthy balance sheets and strong market positions. Those are recipes for success in any market, and particularly in periods of macro deceleration and uncertainty.

Terry Gardner Jr. is Portfolio Strategist and Investment Advisor at C.J. Lawrence. Contact him at tgardner@cjlawrence.com or by telephone at 212-888-6403.