- January 28, 2019

- Blog , The Portfolio Strategist - Terry Gardner

C.J. Lawrence Weekly – Revenue Growers Stand Out

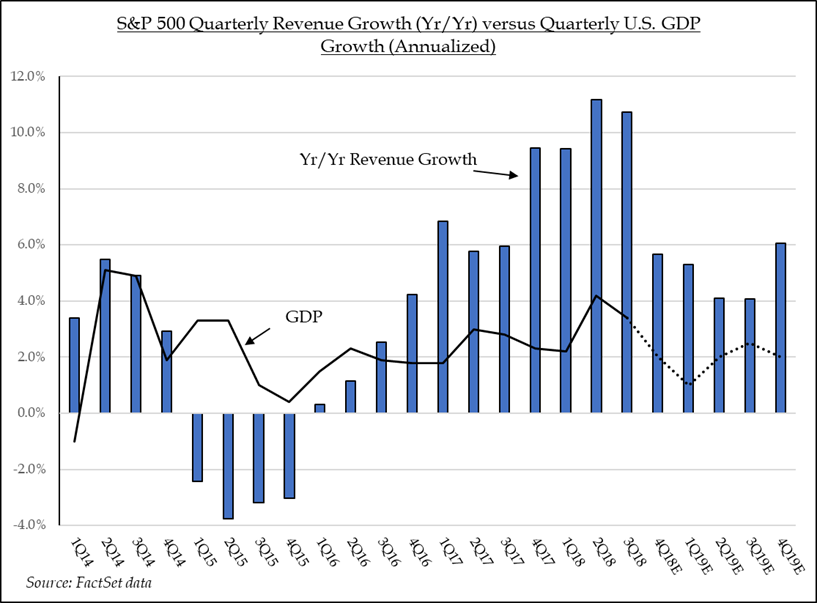

This coming week will be an important one for earnings watchers. 126 of the 500 companies in the S&P 500 Index will report 4Q18 results, including bellwethers like Microsoft, Amazon, and Apple. So far, fourth quarter reports are coming in close to plan. Of the 110 companies that have reported, 71% have delivered earnings results, and 59% have delivered sales results, that exceeded analyst expectations. The earnings surprise figure is equal to the 5-year average of quarterly earnings surprises, while top line surprises are slightly below the 5-year quarterly average.

But perhaps more important than what companies delivered in 2018 will be their business outlooks for the coming year. S&P 500 Index sales and earnings forecasts for 2019 have been coming down steadily for the past several weeks. The U.S. federal government shutdown will likely accelerate 1Q19 downward revisions for companies with direct and indirect businesses exposure to federal workers and installations. Since corporate sales growth typically tracks the direction and magnitude of GDP growth, it is likely that Index top-line growth will be below trend in 1Q19. But even prior to the shutdown, top line growth for the Index was expected to slow by almost 50% from 2018’s level. A good rule of thumb has been that S&P 500 Index revenue growth tends to be 2.0x – 2.5x U.S. GDP growth. If GDP growth slows to 2.0% this year, that would put Index sales up 4.0%-4.5% in 2019. That is below the current forecast of 5.1%

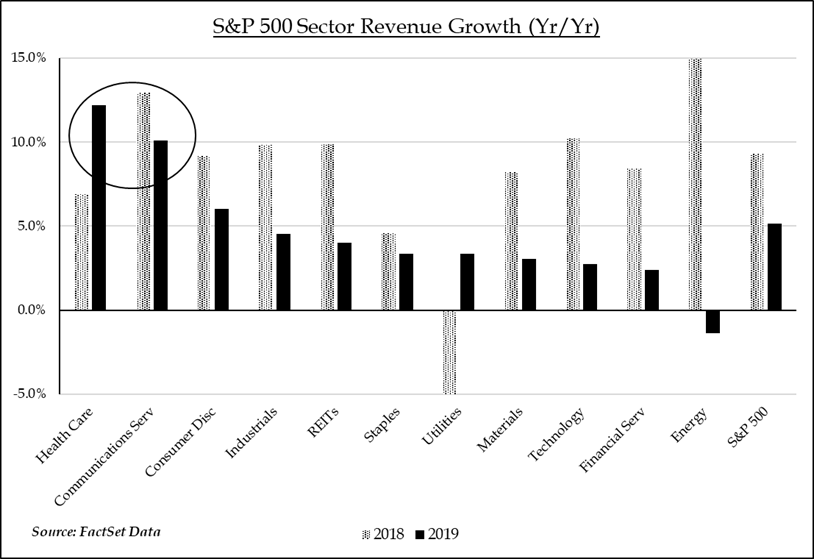

Only one S&P 500 sector is expected to generate accelerating revenue growth in 2019. The Health Care sector is forecast to generate 6.9% in 2018 before accelerating to 12.2% in 2019. The Biotech group (10.4% top-line growth) and Life Science Tools group (17.4% top-line growth) are expected to provide the sector’s leadership. Overweighting sectors with accelerating revenue growth has been a winning investment strategy in past cycles, particularly when S&P 500 sales growth is decelerating. Health care companies with expanding product pipelines, entrenched market positions, healthy balance sheets, and deep research and development capabilities look particularly attractive. Communications Services is the only other sector expected to generate double digit sales growth in 2019, although its 10.1% forecast is below 2018’s anticipated 13% rate. Nonetheless, double digit revenue growth has become a market rarity and is impressive in any cycle. As companies report results and adjust forecasts, increased attention should be paid to companies with attractive top-line growth profiles, expanding market share, and strong competitive positions. That is a recipe for success in any market, and particularly in periods of macro deceleration and uncertainty.

Terry Gardner Jr. is Portfolio Strategist and Investment Advisor at C.J. Lawrence. Contact him at tgardner@cjlawrence.com or by telephone at 212-888-6403.