- May 14, 2018

- Blog , The Portfolio Strategist - Terry Gardner

C. J. Lawrence Weekly – Profit Margin Expansion Suggests Current Business Cycle Has Legs

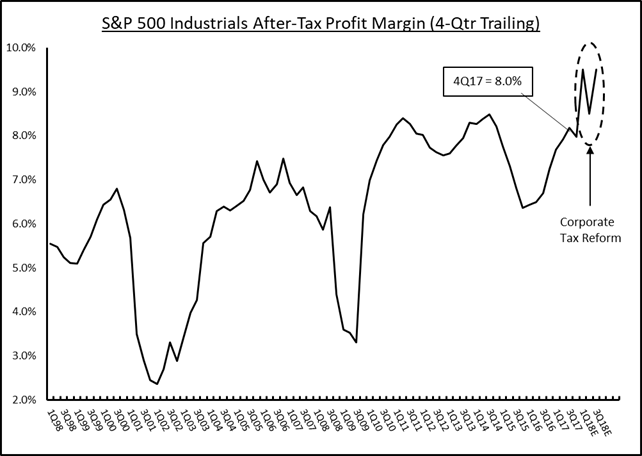

In the late stages of a business cycle it is typical to see profit margins contract in the face of rising input costs and strained revenue growth. But over the past decade, U.S. business efficiency improvements have helped companies avoid the deep margin troughs of past cycles, and sustain historically high profit ratios. In late 2014, aggregate margins on most of the major equity indices looked to be peaking, but got a second wind in 2015 and retraced their expansion in 2016 and 2017. Profit margins on the S&P 500 Industrials Index, which excludes Financials, REITs, and Utilities, are now close to 8.0%, which is approaching the 8.3% calendar year peak achieved in 2013. For the past 50 years the annual profit margin on the S&P Industrials, and its successor index, the S&P 500 Industrials, has averaged 5.5%. Meanwhile, index profit margins broke the 8.0% barrier for the first time in 2011 and have eclipsed that mark, on an annual basis, four times since.

Not only are S&P 500 Industrials Index margins expected to sustain a rate above 8.0% this year, but if estimates prove correct, they will eclipse 9.0%, on a 4-quarter trailing basis, for the first time. The broader S&P 500 Index shows the same progression, with profit margins expected to reach 12.0% this year, up from 10.6% in 2017. The sector contributing most to aggregate margin expansion is the heavily weighted technology sector, which produced a 21.7% profit margin in 2017, versus its 20-year average of 15.3%. Interestingly, the Technology Sector, the constituents of which help others become more productive, is the sector producing the highest organic productivity and profit improvement. Conversely, Consumer Staples margins are below their 2002 peak of 9.4%, and finished 2017 below their 20-year average of 6.6%.

Market consensus suggests that current year margin improvements are being driven primarily by the benefits of corporate tax reform. Indeed, lower rates are an important contributor, but S&P 500 companies are also showing operating improvements above the tax line. EBIT (Earnings Before Interest and Taxes) margins on the S&P 500 are expected to reach 16.6% in 2018, versus 15.8% in 2017, and are expected to expand to 17.1% in 2019 and 17.3% in 2020, according to bottoms-up estimates collected by FactSet. At the same time, top line growth is expected to accelerate in 2018 by 7.2%, and maintain a good growth clip of 4.7% in 2019. This is a constructive backdrop for stocks and suggests that the current business cycle and outlook remain healthy. Meaningful revenue growth combined with expanding margins is a good recipe for profits, and owning stocks with that winning combination is a proven strategy for capital appreciation. The most attractive candidates can be found in the Technology and Industrials sectors which are delivering on both.

Full Disclosure: Nothing on this site should be considered advice, research or an invitation to buy or sell securities, refer to terms and conditions page for a full disclaimer.