- March 12, 2018

- Blog , The Portfolio Strategist - Terry Gardner

C.J. Lawrence Weekly – New S&P Sector Construct Could Create Volatility this Summer

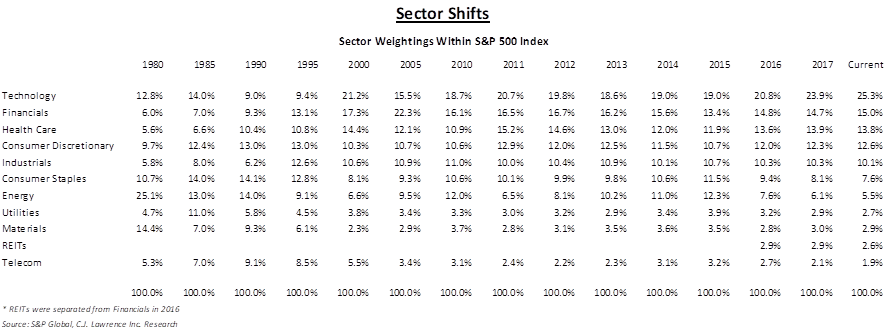

Followers of the CJL Weekly Market Comment are familiar with our practice of looking below the broader market indices to compare the fundamentals, price performance, and valuations of the 11 different S&P Sectors, 24 Industry Groups and, 157 Sub-Industries. This style of analysis dates back to the original C.J. Lawrence. For decades, the firm published tables showing the relative sector winners and losers of market share within the S&P 500 Index. This long-term lens has provided an important perspective to investors utilizing a top-down approach in their securities analysis. Indeed, we continue to consider the changing landscape highlighted in our Sector Shifts table in our investment process.

Standard and Poor’s Corporation, (now S&P Global, Inc) was the developer of the original indices, and is still today the owner, vendor, and licensor of the index data. The indices follow the Global Industry Classification Standards (GICS), a standard developed in 1999 by S&P and MSCI, which allows for the consistent categorization of individual securities. This categorization is relevant because it determines which securities are included in funds and products that track the indices and sub-indices. Periodic index reconstitutions have become important market events as companies are added to, and removed from, the various indices, while derivative product manufacturers react to the changes. One of the larger definitional changes undertaken by S&P in recent years was the separation of the REIT stocks from the Financials sector in August of 2016. Since the split, the Financials Sector Index has delivered a 59.5% total return, while the new REIT Sector Index has produced an -5.7% return during the same period. The post-split impact has been meaningful for index trackers. In November of 2017 S&P announced another major change, to take place this year.

In September, S&P will broaden the Telecommunication Services sector index and rename it Communication Services. Importantly, S&P will remove social and interactive media companies from the Technology sector and add them to new Communications Services sector. The same shift will take place for interactive home entertainment companies. Stocks impacted by the move include the third and fifth largest market capitalization companies in the S&P 500, Alphabet (GOOGL) and Facebook (FB), as well as widely held gaming companies Activision Blizzard (ATVI) and Electronic Arts (EA), among others. Additionally, Broadcasting, Cable and Satellite, Movies and Entertainment, and Publishing stocks will be transferred out of the Consumer Discretionary Sector and will also be added to the Communications Services sector. Traditional hardware and software companies will now dominate the Technology Sector index. To help ease the transition, S&P Global is considering publishing tracking indices that mimic the new construct. But the index changes could ultimately lead to increased volatility this coming summer and fall as index trackers adjust their holdings, and index algorithm creators and traders re-write sequences and code to account for new trading patterns and conditional relationships. There is a frequently run TV and radio commercial that poses the question, “Why own single stocks when you can own the entire sector?” This realignment may be one of the reasons why.

Full Disclosure: Nothing on this site should be considered advice, research or an invitation to buy or sell securities, refer to terms and conditions page for a full disclaimer.