- October 23, 2017

- Blog , The Portfolio Strategist - Terry Gardner

C.J. Lawrence Weekly – Goldilocks’ Porridge Made With Copper and Gold

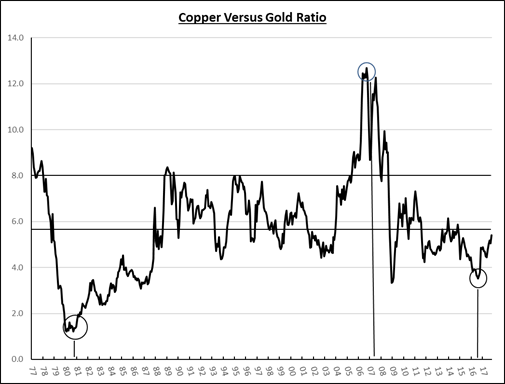

A useful ratio in gauging global growth prospects versus global fear is the copper-to-gold price ratio. The ratio has become increasingly relevant over the past fifteen years as China, now the dominant swing factor in the global growth equation, has emerged as a massive copper consumer. At the end of 2016, China was responsible for almost 50% of global refined copper consumption, according to the World Bank. It is often said that “copper is the metal with a PhD in economics” because it is used so extensively in the industrial economy. Its uses include, but are not limited to, electrical wiring and circuit boards, plumbing, coin production, and metal alloy production. Thus, as economic activity increases, so does demand for copper. Reversals in copper price trends can be important signals for economists, as are significant price increases and decreases relative to other commodities.

Conversely, there are not many industrial uses for gold. In fact, about 78% of new gold production is used to make jewelry. The rest is added to stockpiles held by central banks, speculators, traders, and vaults containing trade collateral and bullion associated with gold-backed securities. Despite its’ limited industrial uses, ownership of the yellow metal is still widely viewed as a hedge against inflation and currency debasement, and for safety-seekers, as a safe-haven in times of geo-political and economic crisis.

At peaks and troughs, the copper-to-gold price ratio can identify important inflection points in the balance between growth and inflation, as it did at the trough in September of 1980 and at the peak in September of 2006. More recently, the ratio troughed in August of 2016, signaling a bottom in industrial commodity prices, and higher global economic growth prospects. The fact that the ratio has increased gradually suggests that the improvement in commodity prices has likely been driven by stronger unit demand, rather than broad based price inflation. Over the past forty years the ratio has averaged 5.8, and has averaged 6.3 over the past 17 years. It now stands at 5.4. Higher, but not inflated, copper prices and consumption are important underpinnings to global growth. The current ratio may be signaling that the current Goldilocks environment for stocks (low inflation and steady, moderate economic growth) may stick around.

Full Disclosure: Nothing on this site should be considered advice, research or an invitation to buy or sell securities, refer to terms and conditions page for a full disclaimer.