- May 29, 2018

- Blog , The Portfolio Strategist - Terry Gardner

C.J. Lawrence Weekly – Growth Stocks Reaccelerate

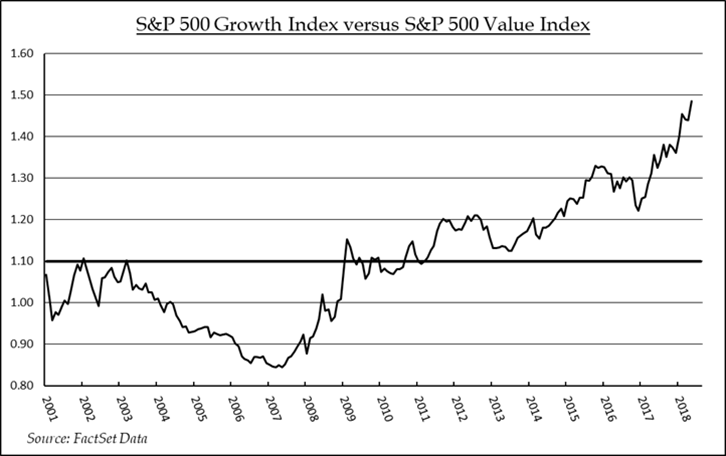

On a relative basis, it has been a challenging decade for value investing practitioners. Since January of 2009, the S&P 500 Growth Index has delivered a 326% total return, while the S&P 500 Value Index returned 212% during the same period. Definitions of what constitutes value stocks and growth stocks differ, but most agree that to qualify as a value stock a company’s shares should trade at relatively lower price-to-fundamentals (earnings, sales, book value, etc.) than the market. Conversely, to qualify as growth stocks, shares should exhibit faster fundamental growth than the market, and typically trade at premium valuations. Traditional value sectors include Energy, Consumer Staples, Telecom, Utilities and Financials. Growth names can typically be found in the Technology, Consumer Discretionary, and Health Care sectors. Industrial stocks can be found in both but tend to tilt towards value.

The cyclical nature of value stock investing makes timing important. But head-fakes can be common. In 2016 it appeared as if growth’s relative outperformance was waning as the mean-reversion trade took hold and value closed the price gap. That looked to be the right trade as economic and corporate profit growth forecasts increased steadily through 2017, bolstering the case for economically sensitive shares. But value’s rally stalled and growth stock prices reaccelerated in 2017 as relative valuation multiple gaps closed. Stronger than expected fundamentals allowed earnings to grow into growth stock multiples, rendering their relative value more attractive. Meanwhile valuations on value stocks had reached historical highs making the “value” case less compelling.

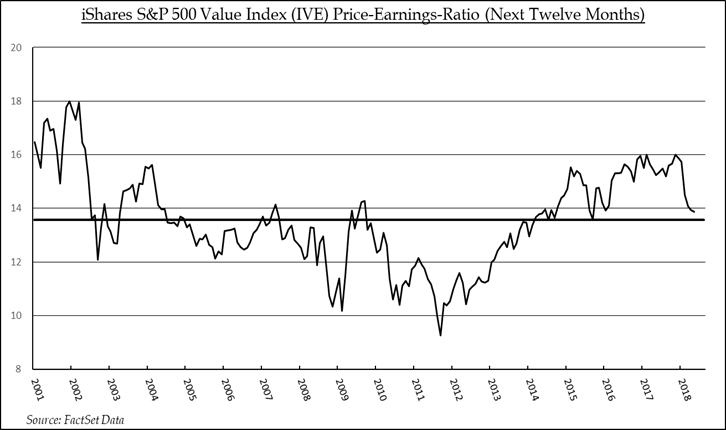

Using P/E multiples to measure the attractiveness of value stocks can be challenging because investors will often award high multiples to cyclical shares at trough earnings, and pay lower multiples for peak earnings. But the relative value analysis can be instructive if peak earnings are not yet in sight, which we believe is the current scenario. Weak financial share price performance, on the back of solid earnings reports and upward estimate revisions, and higher oil prices that have boosted the outlook for energy company earnings growth, have both contributed to the value style’s relative valuation improvement of late. But the value style still has its challenges. Oil and energy company share prices rolled over at the end of last week as talk of increased OPEC production spread through the market. Industrial stocks rallied early in 2018 but fell out of favor as fears of a pending cyclical top percolated. The heavy-weight financial stocks posted strong price performance in 2017 but have lagged the broader market in 2018, despite an improving economy and interest rate environment for lenders. Utilities, Telecom, and Consumer Staples shares lost their allure as bond surrogates in the face of higher interest rates, leaving them to trade on fundamentals alone. While we believe that growth stocks will continue their relative outperformance, some “growth-cyclical” stocks, particularly in the industrial and financial sectors, look attractive, and warrant inclusion in both balanced and growth portfolios.

Full Disclosure: Nothing on this site should be considered advice, research or an invitation to buy or sell securities, refer to terms and conditions page for a full disclaimer.