- January 13, 2020

- Blog , The Portfolio Strategist - Terry Gardner

C.J. Lawrence Weekly – Following the Smart Money May Not Be Such a Good Idea

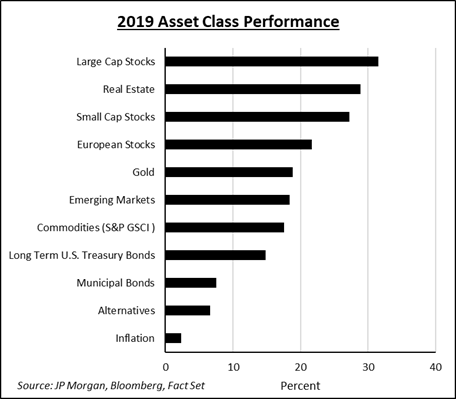

In the coming weeks investment consultants will meet with their pension, foundation, and endowment clients to discuss calendar year 2019 investment performance and proposed asset allocation changes for 2020. The conversations will likely be made easier by strong 2019 performance across most asset classes. But a conundrum exists for plan sponsors regarding allocations to U.S. equities. For most of the past decade institutional funds have sought to reduce their exposure to U.S. stocks in favor of uncorrelated asset classes, mostly within the alternative asset class category (hedge funds, private equity funds, venture capital funds, etc.). In fact, heading into 2019, 68% of the participants in Blackrock’s annual institutional survey indicated they were pursuing that strategy. Almost as many suggested they were increasing their private market exposure including private equity, real assets, and real estate. The moves come as U.S. equities climb again to the top of the traditional asset class performance tables and extend their lead as the top performing asset class of the decade, according to data from Yale Professor Robert Shiller.

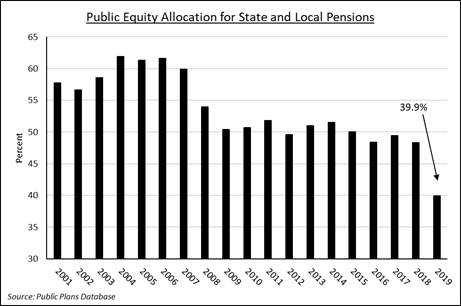

Despite strong asset class returns, equity exposure at state and local pension funds is now at a two-decade low according to data from Public Plans, falling below 40% for the first time in the survey’s history. And equity exposure at most major university endowment funds is reaching record lows. Indeed, according to university reports and Pension and Investments data, target exposure to domestic equities declined to 9% at Princeton University’s endowment fund, 7% at Stanford, and 2.8% at Yale. Harvard disclosed 20% exposure to global equities, but its domestic equity exposure is believed to be below 10%.

Source: Public Plans Disclosure

In addition to pursuing timely asset class shifts, fund consultants and experts face the challenge of comparing valuations of private versus public asset classes. Private equity and venture capital funds lack standardization in valuing portfolio companies, making comparisons among funds and fees difficult. But that isn’t slowing capital flows into the asset class. U.S.-based private equity firms raised more than $300 billion for new funds in 2019, according to data from PitchBook. That total, which is a record, tops the $241 billion raised in 2016, and is a 52% increase from the $198 billion raised in 2018. Pension, foundation, and endowment funds are often referred to as the market’s “smart money”, owing to their resources and expertise, and the smart money has been consistently reducing equity exposure to fund entrée into new and diverse asset categories. To date, returns suggest that betting against equities has been a losing wager. Perhaps the anti-equity pendulum has swung too far.

Terry Gardner Jr. is Portfolio Strategist and Investment Advisor at C.J. Lawrence. Contact him at tgardner@cjlawrence.com or by telephone at 212-888-6403.