- January 6, 2020

- Blog , The Portfolio Strategist - Terry Gardner

C.J. Lawrence Weekly – 2019 Didn’t Feel Great, but It Was!

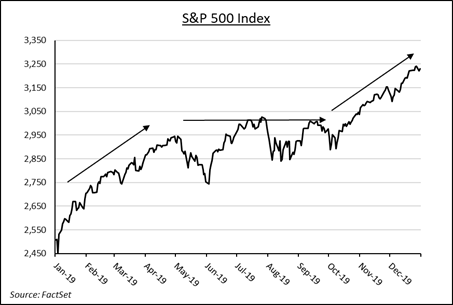

What a difference a year makes! In the week leading up to New Year’s Day in 2018 not many pundits were forecasting that 2019 would produce one of the highest annual equity returns on record. At 28.9%, the 2019 price return on the S&P 500 is the fifth highest since 1960. But at the beginning of the year, the market was standing on shaky legs, having fallen nearly 20% between its October 3rd peak and Christmas Eve. The market narrative around that time was for a slowing global economy and rising risks of recession. It took the first five months of 2019, and a precipitous decline in interest rates, to calm the equity markets, retrace the late-2018 decline, and regain the October 2018 peak. But the rally stalled there. Over the next five months, from May through October, the market generated negligible equity price gains. The S&P 500 Index price rose only 0.5% during that period. But it regained its mojo in October and posted an 8.5% gain between October 1 and the final trading session of the year. For traders, the directionless market presented day-to-day challenges. For longer term investors, patience was challenged but was ultimately rewarded.

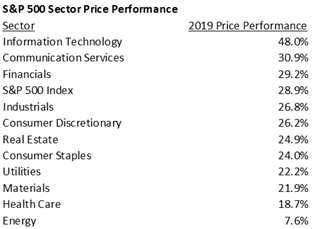

Technology was the best performing sector for the second time in the past three years. A surge in semiconductor equipment and hardware stocks propelled the sector into the leadership position in the back half of the year. Communications Services and Financials rounded out the top three. Significant gains in social media and internet business stocks combined with a resurgence in heavyweight Disney’s stock price propelled the Communications Services sector index higher, while the Financial Services sector bucked the trend of lower interest rates to finish the year with a 29.2% price gain. No major sectors were down for the year and Energy was the only sector to finish 2019 with a single digit gain.

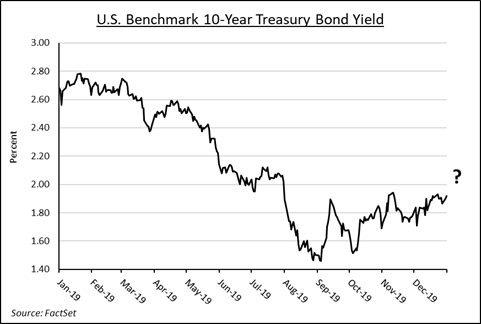

Dovish U.S. monetary policy and low/negative global interest rates created little competition for stocks in 2019, yet capital continued to flow out of equities and into bonds. Meanwhile, low inflation allowed price-earnings multiples on stocks to climb. Despite a 6.0% decline in S&P 500 2019 earnings per share forecasts between the beginning and end of the year, the price-earnings multiple on the S&P 500 expanded by 37.1% during the same period. In 2020, earnings per share are expected to improve by 9.6%, according to FactSet, but a case for further multiple expansion is tough to make. Thus, a high single digit return on the index seems plausible for 2020 given the earnings outlook. Higher interest rates, should they materialize, or geo-political events, could upset the mix and weigh on the price-earnings multiple that was so supportive of stocks in 2019. In that case earnings will need to show resiliency for the market to move higher.

Terry Gardner Jr. is Portfolio Strategist and Investment Advisor at C.J. Lawrence. Contact him at tgardner@cjlawrence.com or by telephone at 212-888-6403.