- June 10, 2019

- Blog , The Portfolio Strategist - Terry Gardner

C.J. Lawrence Weekly – Will China Bite the Apple?

The stock market, as measured by the S&P 500 Index, shrugged off a disappointing payroll report and ongoing concerns about U.S. – China trade relations, to post an impressive 4.4% gain last week. The 10-year U.S. Treasury Bond yield returned to playing a supporting role in the market’s advance, with the yield closing the week at 2.08%, down 6 basis points in the period, and down 37 basis points in the last month. Dovish comments from Fed Governors gave market watchers increased confidence that the next move by the Fed will be to lower interest rates. In fact, after the employment report was released, the Fed-Funds futures moved markedly higher, signaling market expectations that the Fed would likely reduce the Fed-Funds target rate by 25 basis points by the end of July, and perhaps 50 basis points by September. Equity analysts have been slow to lower earnings forecasts for this and next, but the bond market is already signaling meaningfully slower growth ahead, catalyzed by lower global trade activity.

The market may breathe a sigh of relief that higher tariffs on Mexican goods are not going into effect, for now. But the tension between the U.S. and China does not look to be going away any time soon. Some economists are speculating that the framework for a new deal could be discussed between President Trump and President Xi Jinping during the G-20 Summit in Japan at the end of June. But in the interim, both sides are moving forward with measures that could have a lasting impact. The recent fines levied on Ford’s China joint venture, and the ongoing investigation into FedEx for the misdirection of four Huawei packages have soured the mood of U.S. companies doing business in China. Two weeks ago, in a “random” sweep of China-based trade organizations, the American Chamber of Commerce in China was selected for inspection and review. This all comes ahead of the Chinese government’s release of its “unreliable entities list” which will identify foreign “persons and organizations that do not follow market rules, violate the spirit of contracts, or blockade and stop supplying Chinese companies for non-commercial reasons.”

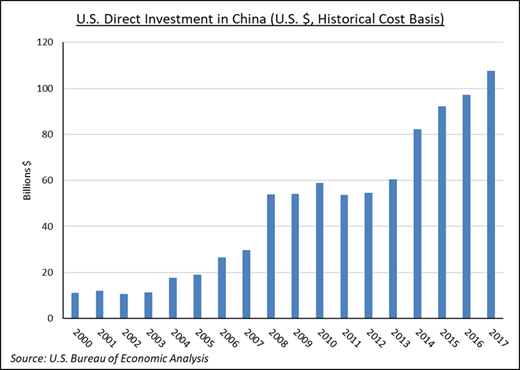

The composition of the unreliable entities list should give us a good indication of how far China is willing to go in its trade battle with the U.S. While we wouldn’t expect Apple to be on the list, it is a marquee U.S. brand, and its treatment by the Chinese government bears watching. Apple, which has substantial production and assembly operations in China derives ~20% of its revenues from the domestic Chinese market and the company claims that its ecosystem supports 4.8 million jobs in China. Any explicit, or implicit, targeting of Apple’s business or supply lines would send a loud message to the U.S., but would also have a deleterious effect on the local economy surrounding Apple’s China ecosystem. Targeting Apple could be a signal that the Chinese government is willing to endure a high level of local discomfort in order to send the message that it intends to sustain its current business modus operandi. Thus, if China is willing to bite the Apple, the odds are high that the current trade dispute could move to a whole new level, and that would be another negative development for the global economy and for equity markets.

Terry Gardner Jr. is Portfolio Strategist and Investment Advisor at C.J. Lawrence. Contact him at tgardner@cjlawrence.com or by telephone at 212-888-6403.