- October 31, 2017

- Blog , The Trusted Navigator - Bernhard Koepp

American Renaissance in Manufacturing: Fact or Fiction?

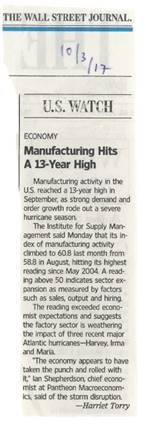

Those of you who still read the daily newspapers in print, will have noticed a small article buried away in the back pages of the Wall Street Journal on October 3rd which did not get enough attention in my opinion. The title was “Manufacturing Hits a 13-Year High”. This fact did not escape our good friend Ed Hyman at Evercore ISI, Wall Street’s most relevant economist by a mile, who taught us that when US-Manufacturing is on the rise, despite being a relatively small part of the overall economy, it is usually associated with higher real GDP growth in the future.

Friday’s Q3 GDP data with a 3-handle in front of it was a sign that the US-economy is on the move. Pessimist point to an inventory build which may be temporary, but it is a confirmation that the economy is accelerating.

Friday’s Q3 GDP data with a 3-handle in front of it was a sign that the US-economy is on the move. Pessimist point to an inventory build which may be temporary, but it is a confirmation that the economy is accelerating.

In 2013, I launched the American Renaissance Portfolio at our predecessor firm ISI Group Inc., as an investable basket of about 60 stocks benefiting from this nascent trend. Inspired by Nancy Lazar’s great macro work then at ISI (now at Cornerstone Macro) we identified a universe of companies that benefitted from three underlying growth drivers:

- A resurgence of US competitiveness

- Favorable labor cost demographics (relative to other OECD countries)

- Access to low cost domestic energy

These three characteristics were a tough sell in 2013 when we were more concerned about government shut-downs and the blow back from the great recession. It seemed unreal then that the US shale revolution could grow US production to rival that of Saudi Arabia’s. Stocks that participate in the American Renaissance can be found not only in the traditional industrial and manufacturing sectors, but also include housing, infrastructure, domestic rails, petro-chemicals, regional banks, defense contractors, and of course local energy producers.

Today the debate rages among politicos about who gets credit for the “Trump trade” or what Keynes referred to as the unleashing of “animal spirits”. There is a consensus building among economists that the train has left the station and we are well on our way to normalizations. Lift off may be just around the corner. There is no doubt that despite being 8 years into an equities bull market, we are still early in the economic cycle. What this means for investors is to be aware of a thematic shift to American Renaissance type stocks. Portfolio strategists will use concepts like sector rotation to value or shift to smaller size, and reflation to describe the same phenomena. It is a fact, that American Renaissance stocks tend to be smaller, more skewed to value sectors and certainly do well when inflation is on the rise, so get on board for the ride!

Full Disclosure: Nothing on this site should be considered advice, research or an invitation to buy or sell securities, refer to terms and conditions page for a full disclaimer.