- November 26, 2018

- Blog , The Portfolio Strategist - Terry Gardner

C.J. Lawrence Weekly – Checking the Pulse of the Freight Economy

The shift in economic and market sentiment during the past few weeks has been palpable. The once synchronized global growth chorus has subsided and has been replaced with a negative refrain of global growth deceleration. Recent lackluster economic data releases from China and Europe have contributed to growing pessimism. In conjunction with downward foreign GDP estimate revisions, economists have ratcheted down expectations for 2019 U.S. GDP growth in conjunction with slowing international trade. Some economists have gone as far as to forecast a U.S. recession in the next 12-18 months. Analysts who contribute to the FactSet consensus estimate for the S&P 500 Index are not aligned with that positioning. 2018 earnings expectations are down only 0.8% from their peak, and 2019 estimates are down only 0.4% from their peak. The market has reacted to the economy-versus-market tug-of-war by reducing the P/E multiple investors are willing to pay for 2019 S&P 500 earnings per share from 16.6x at the beginning of the year, to its current level of 15x, despite a 3.5% increase in estimates. Freight flows are often good indicators of the direction of economic activity and are currently giving some mixed signals.

The Baltic Dry Index measures the price of shipping raw materials such as metals, ores, and grains by sea. The largest category of ship tracked by the BDI is the Capesize class. It was given its name because the ship’s size precludes it from transiting the Panama Canal, necessitating shipping routes that circumnavigate the Capes of Good Hope and Horn. Demand for Capesize capacity is closely tied to the health of Chinese commodity demand. Rates for these ships are down 70% since August. The broader BDI is down 38% from its August peak and is down 31% from this week last year. Meanwhile, global air cargo traffic is still growing but current growth is below trend. The International Air Transport Association (IATA), reported global air cargo traffic up 2.0% in September and up 2.3% in August, which are both below the five-year average growth rate of 5.1%. Estimates for October, due out next week, suggest a consistent pattern. October data from the Hong Kong International Airport, a major global cargo transshipment facility, showed a 2.8% increase in international freight tonnage in October, versus that same period last year.

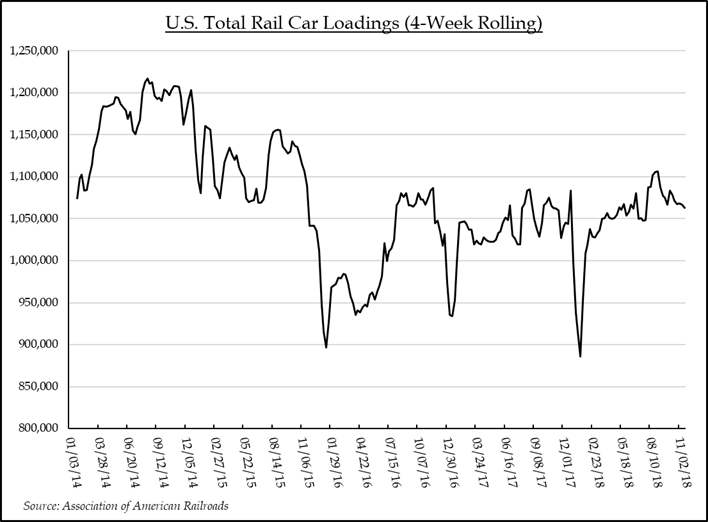

US Total Rail Car Loadings (4-Week Rolling) | Source: Association of American Railroads

The domestic freight landscape looks markedly better. Rail traffic, on a rolling four-week basis, is surging on the back of strong petroleum and grain shipments. Intermodal traffic (rail shipments of containerized cargo) is up 2.3% on a four- week rolling basis, versus the same period last year. Truck traffic remains strong with the American Trucking Association reporting a 9.5% increase in total tonnage in October versus the same period last year. The Cass Freight Index, which measures a different sample of U.S. shippers than the ATA, showed shipments up 6.2% in October. These reports highlight the relative strength of the U.S. domestic economy versus other industrial economies and provide a good barometer for economic activity at home and abroad. While the U.S. freight economy appears buoyant, a continued slowdown in global activity will likely weigh on domestic indicators in the months ahead. The bright spot in the freight traffic mix continues to be U.S. to U.S. trade where healthy domestic consumers and companies are transacting with each other at high levels. Investors looking for attractively priced equity market opportunities amid current volatility would be well served to follow the freight flows.

Terry Gardner Jr. is Portfolio Strategist and Investment Advisor at C.J. Lawrence. Contact him at tgardner@cjlawrence.com or by telephone at 212-888-6403.