- December 18, 2017

- Blog , The Portfolio Strategist - Terry Gardner

C.J. Lawrence Weekly – Time to Rotate to Value Stocks?…Not So Fast

The likely passage of the U.S. tax reform bill, a bump up in the U.S. Fed Funds target rate, and better than expected economic data have all contributed to a reevaluation of equity investor sector and style weightings. As discussed in last week’s note, we got a glimpse of rapid sector rotation two weeks ago when the U.S. Senate announced it had the requisite votes to move on tax legislation. The shift from growth to value, or in this case, from less tax-advantaged to more tax advantaged, was fast and furious. But interestingly, much of that rotation reversed itself over the past two weeks, calling into question the permanency of the shift.

Periods of accelerating economic growth have historically been good backdrops for value stocks. The thesis holds that value stocks are more sensitive to changes in economic activity and typically trade at lower valuations, so they can be bought early-cycle at discounts, and outperform during the expansion. For “style box” allocators, the debate centers on whether now is the right time to undertake a meaningful tactical shift and overweight value stocks in equity portfolios. Rules-based investors, who continuously rebalance their portfolios according to preset asset allocation and style weight targets, have underperformed over the past several years as they sought to stay within their style guidelines while growth stocks vastly outperformed. Since 2010, the growth style, as measured by the S&P 500 Growth Index, has outperformed value, as measured by the S&P 500 Value Index, by over 50%. Mean reversion advocates suggest, therefore, that the environment is ripe for a reversal, and for the two styles to come back in balance. Technicians are echoing that call based on what they see as extended price action in many growth stock categories. But the fundamental picture paints a different story.

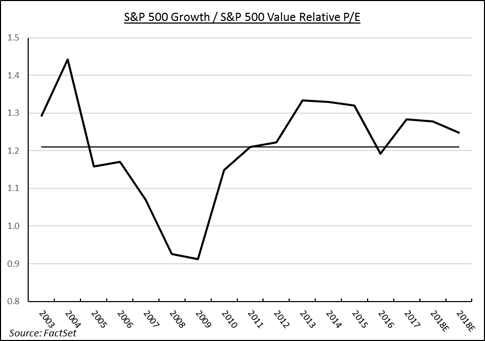

S&P 500 Growth / S&P 500 Value Relative P/E

To categorize stocks as either growth or value, Standard and Poor’s uses formulas that score stocks on the following criteria: price/earnings ratio, price/book value ratio, price/sales ratio, three-year earnings growth, three-year sales growth, and price momentum. In some cases, a single stock may show up in both indices, but its weighting is often meaningfully different in each. At this stage in a bull market one might expect that growth stock valuations would far exceed those of value stocks, especially given the price differential experienced over the past several years. But interestingly, growth stocks look cheaper on a relative value basis than they have since 2013. Over the last 15 years, growth stocks have traded at a 1.21 relative P/E to value, having peaked at 1.44 and troughed at .91. That ratio now stands at 1.28 and has been declining since 2013. The same holds true for price/book value, return on equity, and price/earnings growth (PEG) relative comparisons. The technical set up may be giving a green light for a rotation from growth to value stocks, but historical fundamental valuation comparisons are telling growth weighted managers to stay put.

Full Disclosure: Nothing on this site should be considered advice, research or an invitation to buy or sell securities, refer to terms and conditions page for a full disclaimer.