- June 17, 2019

- Blog , The Portfolio Strategist - Terry Gardner

C.J. Lawrence Weekly – S&P 500 Earnings Forecasts are Heading Lower. Can the Market Handle It?

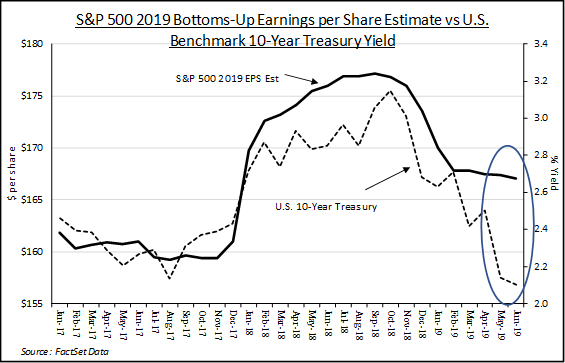

The S&P 500 posted another positive performance last week and is now within 2% of the Index’s record high set back in April. Last week’s U.S. economic reports were generally supportive. Retail sales for May came in close to expectations and prior months’ results were revised upwards. U.S. Industrial Production and Capacity Utilization came in slightly ahead of expectations, relieving some of the gloominess surrounding recent trends in those data sets. The bond market, however, did not find much to celebrate in the data pushing the yield on the U.S. 10-Year Treasury Bond down another 4 basis points to finish the week at 2.09%. Lower yields tend to support stock prices, but at some point, declining yields also begin to flash a warning sign for corporate profits.

The bond market may be incorporating a broader view of the world than the U.S. stock market. While U.S. economic data remains generally supportive, much of the data flow from other parts of the world is not. The impact of slowing global trade and general economic malaise in Europe are evident in recent releases. Last week China reported healthy domestic May retail sales growth of 8.6%, but the country also released a report showing the slowest industrial production growth in 17 years. Japanese machine tool orders were up for the month of May but are down a whopping 27% from last year’s level. German industrial output dropped 1.9% in May, the sharpest decline since August 2015. German exports fell 3.7%, also the biggest drop since August 2015. Of course, these are just a few anecdotes, and other data may look more favorable. But broad negative sentiment is reflected in global sovereign bond yields which are back to historic lows. Eurozone, Japanese and German 10-Year bond yields are all negative. The US 10-Year continues to be the nicest house in a bad neighborhood but the continued flattening of the long end of the yield curve may be foretelling a downgrade in U.S. economic forecasts.

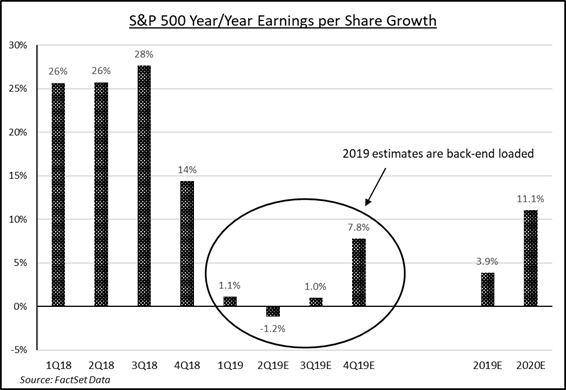

Historically, the 10-year treasury yield and corporate earnings have been directionally correlated. As yields rise so do expectations for higher profits, and vice versa. If the yield curve is right, corporate profit estimates are too high. Analysts may be waiting for 2Q19 results and new management guidance before recalibrating earnings models, but the likely outcome is that aggregate forecasts are heading lower. Broadcom may have given us a preview of the 2Q19 earnings report narrative last week with its top and bottom line fiscal 2nd quarter miss and meaningful forecast downgrade. The semiconductor company’s business is highly exposed to China’s production of electronics and to Huawei in particular, so the magnitude of the downgrade is understandable. But the storyline of slowing global demand and uncertainty is likely to be a recurring theme this earnings season. The challenge for investors will be to judge whether these issues are lasting or transitory. Current bottoms up forecasts from Fact Set call for the S&P 500 to deliver 3.8% earnings growth this year, bolstered by a strong 4th quarter result. Should analysts pull in their horns for the fourth quarter, odds rise that the S&P 500 will experience the index’s first full year negative earnings comparison since 2015. For now, the stock market seems to like the prospects for lower interest rates. But if the bond market is right, corporate profits are headed lower and investors will have to grapple with the balance of lower rates and declining profits.

Terry Gardner Jr. is Portfolio Strategist and Investment Advisor at C.J. Lawrence. Contact him at tgardner@cjlawrence.com or by telephone at 212-888-6403.