- May 21, 2018

- Blog , The Portfolio Strategist - Terry Gardner

C. J. Lawrence Weekly – Healthy U.S. Consumer is Bullish for Consumer Discretionary Sector Leaders

After a difficult second half of 2017, the S&P Consumer Discretionary sector index has staged an impressive comeback. In the past six months the sector price index is up 12.1%, 6.9% ahead of the broader S&P 500 Index. Over the past several years, the bull-bear battles within the sector have limited the advance of many of its constituents, despite headline sector outperformance. Most of those battles have been centered around the brick and mortar retail groups and investor fears that stock price advances among leaders will be limited by the persistent overhang of the “Amazon-effect”. Even headlines suggesting that Amazon might consider entering a new category have caused sell-offs. The battles have touched almost all the sector’s sub-indices including; Auto Parts, Leisure Products, Media, and Household Durables. Interestingly, while Amazon’s shadow has cast a pall over its fellow sector constituents’ stock prices, its own heavily weighted shares have, at times, carried the entire sector price index on its back. Amazon’s parent industry group, Internet and Direct Marketing Retail, is up 36% year-to-date. But better-than-expected results last week from Macy’s and Walmart, may have assuaged some investor fears that retail is a zero-sum game, and raised the specter that “peaceful” coexistence is a possibility. While the picture of the future retail landscape remains cloudy, and ambiguity around international trade adds to the uncertainty, it is likely that, in the near term, retail and the broader Consumer Discretionary sector will be supported by a healthy U.S. consumer.

Last week’s positive retail company financial results came on the back of Tuesday’s U.S. Retail Sales report from the Commerce Department, which showed a headline gain of 0.3% in April, consistent with most economists’ estimates, and raised the previously released March result to 0.8%, well ahead of expectations. The retail-control group sales, which are used to calculate gross domestic product (GDP) and exclude food services, auto dealers, building materials stores and gasoline stations, improved 0.4% after an upwardly revised 0.5% March gain. Retailers are optimistic, and the winning streak looks like it will continue. A recent Global Port Tracker report from the National Retail Federation, which measures shipping container traffic coming into U.S. ports, pointed to robust container shipping activity. According to the report, in April, US ports handled an estimated 1.73 million Twenty-Foot Equivalent Units (TEUs) of incoming cargo, an increase of 6.4% over the prior year period. A TEU is one twenty-foot long container, or its equivalent. May shipments are forecasted to reach 1.82 million TEU, up 4.3% from last year, and June is expected to come in at 1.82 million TEU, a year-over-year increase of 6.1%. Annual shipment growth for July and August traffic is expected to come in at 5.5% and 4.6% respectively.

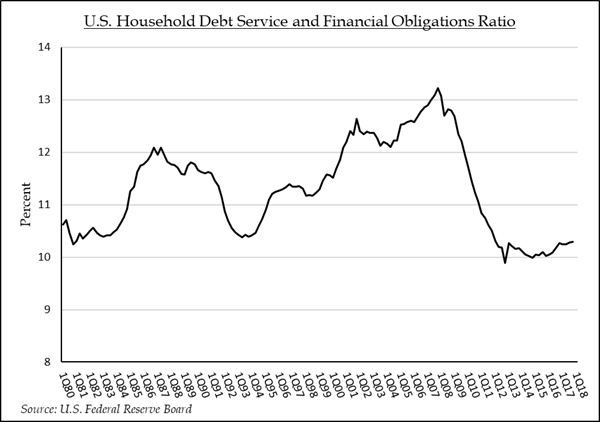

The healthy pace of retail sales, and historically high readings for Consumer Confidence and Consumer Comfort, bode well for U.S. GDP growth, 65%-70% of which is driven by U.S. consumer spending. Some observers have suggested that the consumer is extended and that the current level of consumer spending is debt-fueled and is unsustainable. But a relevant analysis conducted by the U.S. Federal Reserve Board suggests that is not the case. At the end of each quarter, the Fed publishes a measure called the Household Debt Service and Financial Obligations Ratio. The ratio measures household debt as a percentage of household disposable income. While U.S. households have taken on increasing amounts of debt in recent years, disposable personal income growth has outstripped it. In fact, the ratio is at multi-year lows. This is a supportive backdrop for companies in consumer businesses, and is bullish for select leaders in the Consumer Discretionary sector.

Full Disclosure: Nothing on this site should be considered advice, research or an invitation to buy or sell securities, refer to terms and conditions page for a full disclaimer.