- July 12, 2016

- News & Media

The Stock Market’s New High: A Record About Nothing

On the Wall Street Journal’s Moneybeat, Terry Gardner warns Wall Street getting excited about the S&P 500, pointing out the imbalance of the current US stock market.

By Paul Vigna / Jul 12, 2016 10:43 am ET

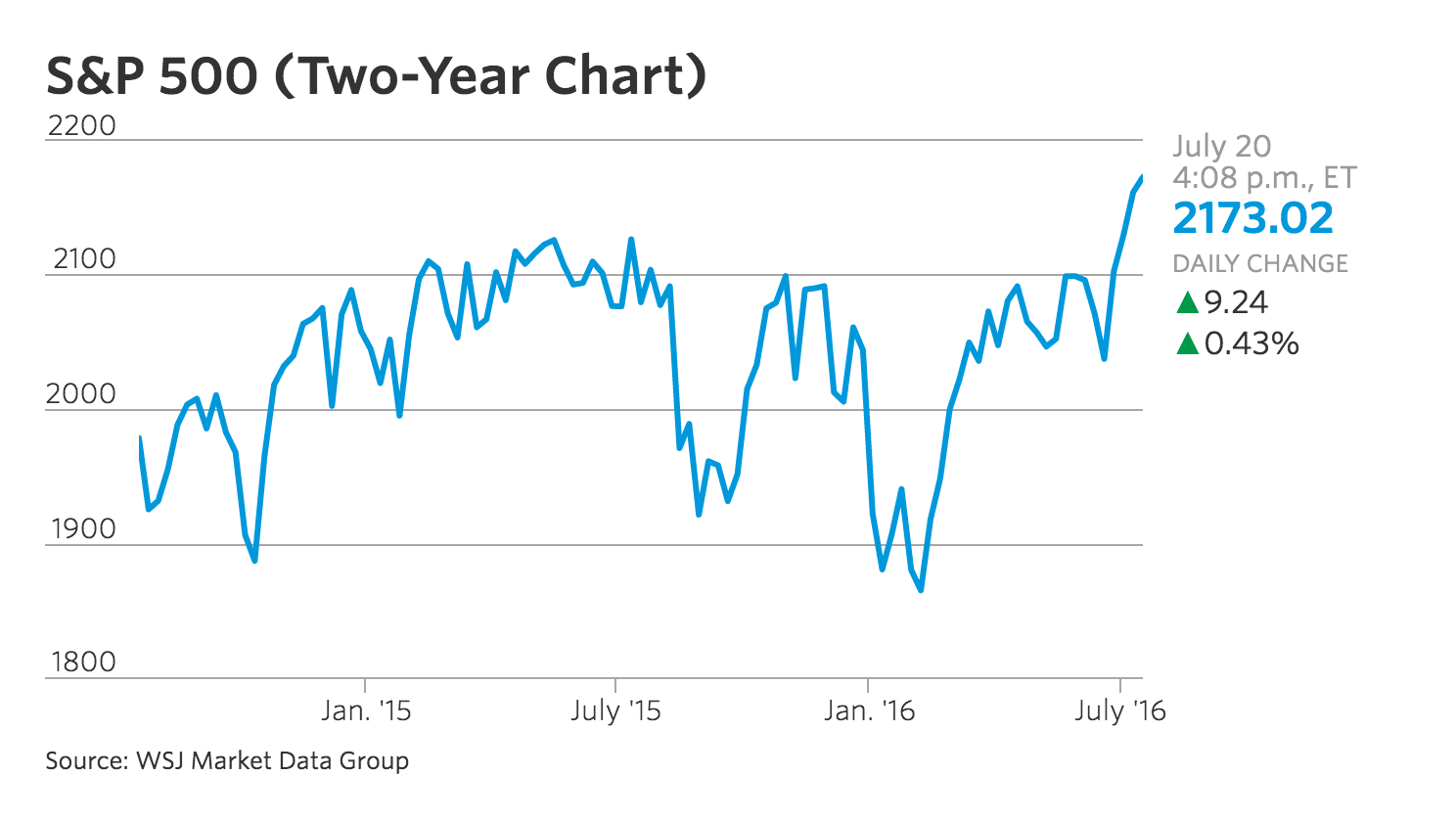

Wall Street’s getting giddy again, with the S&P 500 yesterday, and the Dow today, back in record territory. In the long view, it’s not much to get excited about, really: the S&P 500 is up less than 20 points since its May 2015 high.

Small matters like that aren’t likely to derail today’s “Everything is Awesome” mood on the Street. Yet, for a number of reasons, this is a rally unlike any we’ve seen, and when you look at the guts of it, there is far less to be excited about.

“The rally in stock prices to new record highs is somewhat reminiscent of a Seinfeld episode. It is happening because not much is happening other than interest rates are at record lows,” Ed Yardeni of Yardeni Research wrote. The low rates on government bonds are making yields in the equities market especially attractive, illustrated by the fact that the most interest-rate sensitive sectors – utilities, telecom, consumer staples – are seeing the best returns.

That certainly makes more sense than assuming this rally is based off growth prospects. The equity rally is happening despite the fact that profit growth for the companies in the S&P 500 are expected to have contracted for a fifth consecutive quarter. Despite the fact that Italy is looking at a full-fledged banking crisis. Despite the fact that the real work of the U.K. extricating itself from the EU has not even begun. Despite the fact that the U.S. economy is expected to grow just 2% this year, and the global economy just 2.2%.

Moreover, the latest rally is coming as the pool of available stock has shrunk considerably over the years, a supply-demand imbalance that own its own explains a great deal.

“In 1997 there were over 8,000 publicly traded exchange-listed companies,” C.J. Lawrence strategist Terrence Gardner noted. “That is now below 4,000.” At the same time, companies have been buying back their own shares at a record pace, further reducing the availability of shares available to the public for purchase.

With global asset allocations favoring U.S. equities, investors are finding a smaller market in which to invest

he said.

That supply-demand imbalance may be keeping a bid under some U.S. stocks.

The story is the same, in fact, in the bond market, where massive central bank intervention has hoovered up most of the supply, leaving investors scrambling for a piece of what’s left. “It’s very likely, in my view, that the Fed has thus engineered bubbles in both bonds and stocks at the same time,” money manager Jesse Felder wrote in his Felder Report. That’s led to what he called the “greatest dichotomy in the history of financial markets” – rallies in both the stock and bond markets at the same exact time.

That’s where we are: a world with weak growth prospects, and a bond and stock market with the same level of demand, and smaller pool of supply. Add all that up, and what do you get? About 20 points added to the S&P 500 in 14 months. When you consider the backdrop, it kind of makes sense. It’s just nothing to get giddy about.