- March 19, 2018

- Blog , The Portfolio Strategist - Terry Gardner

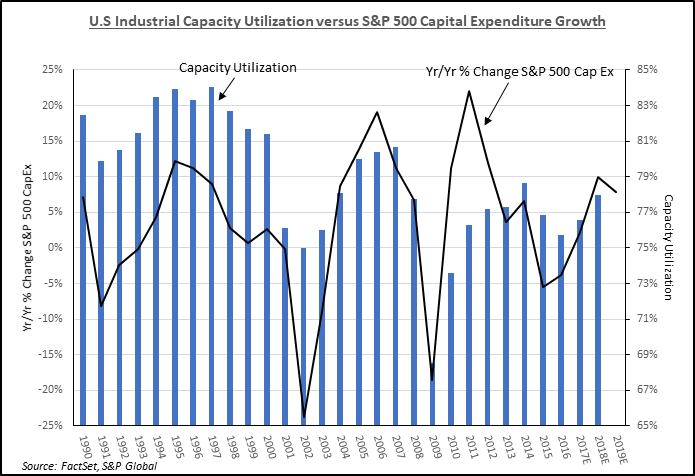

C.J. Lawrence Weekly – Tight Capacity Utilization Bodes Well for Select Machinery, Building Products, and Construction Equipment Stocks

Among the economic data released last week, both Industrial Production and Capacity Utilization came in well ahead of economists’ expectations. The Industrial Production reading, a measure of total U.S. factories, mines, and utilities output, rose 1.1% from the prior month, and 4.4% from last year’s figure. Capacity utilization reached 78.1%, the highest level since January 2015. The two metrics tend to go hand-in-glove. As manufacturing activity accelerates, idle and underutilized manufacturing capacity is re-engaged and the utilization rate climbs. Most economists believe that 80% is an important utilization hurdle. When the utilization rate climbs above that level, and available manufacturing capacity is tight, firms increase capital expenditures on new productive capacity. It appears we are closing in on that trigger level.

US Industrial Capacity Utilization versus S&P 500 Capital Expenditure Growth Source: FactSet, S&P Global

Conversely, utilization, and corporate spending on plant, property, and equipment, falls off dramatically towards the end of, and in the aftermath of, recessions, as orders cancelled during recessions hit the books. Then, in subsequent years, utilization ramps and capital spending re-accelerates, off a lower base, and compensates for the prior spending lag and pent-up demand. Indeed, S&P 500 company capital expenditures fell 24% in 2002 and 9% in 2003 in the aftermath of the 2001 recession. It took almost three years for expenditures to return to pre-recession levels. Likewise, S&P 500 capital spending fell 19% in 2009 and took until 2011 to return to pre-crisis levels. What’s unique about the current economic cycle is that since 2012, capital spending growth, among S&P 500 constituents, has been punk. In fact, there has been no net growth in S&P 500 capital expenditures over the past four years. In 2015 and 2016 capital expenditures declined by 5.5% and 3.8%, respectively, and look to have recovered only modestly in 2017.

Thus, the strong Industrial Production and Capacity Utilization reports are welcome news for investors betting that the current economic cycle has long legs, and that the domestic economy is on the cusp of a new capital spending cycle. Healthy corporate profit growth, fiscal stimulus, and relatively low interest rates are combining with rising utilization, pent up capital spending demand, and healthy corporate balance sheets to form a potent manufacturing brew. Industrial stocks are the likely beneficiary of this convergence, and came out of the gate strong in the beginning of 2018, but have ceded ground on a relative basis over the past two months. While the stocks have largely anticipated the reacceleration in economic activity, some groups look to be discounting peak earnings and have experienced multiple compression. Those groups, including Building Products and Construction and Engineering, in addition to select Machinery and Construction Equipment names, may warrant another look, as the next capital spending cycle gets into gear.

Full Disclosure: Nothing on this site should be considered advice, research or an invitation to buy or sell securities, refer to terms and conditions page for a full disclaimer.